Mortgage Debt Service Ratio

Mortgage payments as share of household income

What is the current Mortgage Debt Service Ratio?

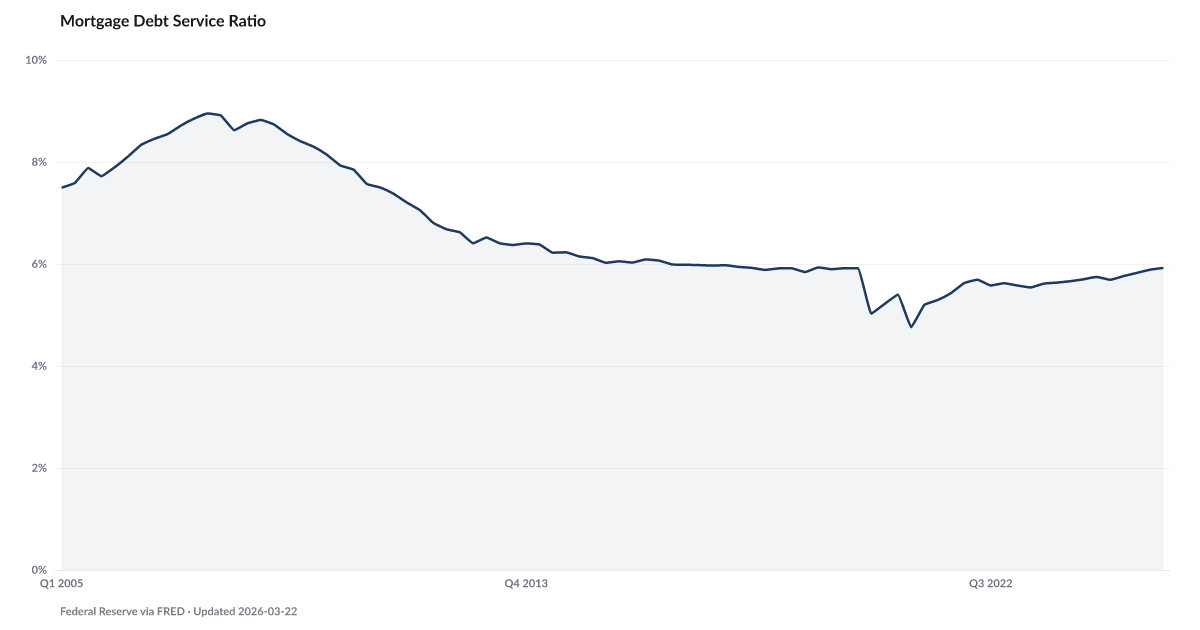

The mortgage debt service ratio isolates the share of household income consumed specifically by mortgage payments. This measure helps distinguish between mortgage-related stress and non-housing debt stress, which have moved in different directions in the current cycle. Source: Federal Reserve via FRED.

Mortgage payments now claim 5.9% of disposable income. Up from the 2021 low, though still well below the 9.0% high reached at the top of the 2007 housing cycle.

The Federal Reserve's Mortgage Debt Service Ratio, FRED series MDSP, measures household mortgage payments as a share of disposable income. The Q1 2026 reading is 5.9%. That's up from a 4.7% low in early 2021, at the bottom of the pandemic rate-cut cycle. The pre-Great-Recession high, in late 2007, was 9.0%.

The increase reflects a specific mechanic. Existing mortgage holders locked in sub-4% rates during 2020 and 2021 and are still carrying them. New originations priced off 7% rates are entering the stock slowly. The average rate on outstanding mortgages has crept up one basis point at a time as the payment share rose with it.

An increase off the bottom sounds dramatic. In context, it barely registers — because the starting point was historically low. That is what makes the pre-GFC comparison misleading. The gap from today to 9.0% measures the distance between a stock of borrowers locked into cheap debt and a future stock of borrowers paying market rates on everything. Not headroom. Pipeline.

As the stock of outstanding mortgages changes through home sales, new originations, and refinancings, the payment-to-income ratio can change too. Read it alongside The Squeeze, The Safety Net, and Falling Behind as separate household-pressure measures, without treating one as a validated forecast of another.

Explore Further

How has Mortgage Debt Service Ratio changed over time?

Most affected counties

Counties with the highest safety net and buffer scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q1 2026 | 5.88% | +0.1 pts |

| Q4 2025 | 5.92% | +0.2 pts |

| Q3 2025 | 5.87% | +0.1 pts |

| Q2 2025 | 5.83% | +0.1 pts |

| Q1 2025 | 5.76% | +0.1 pts |

| Q4 2024 | 5.69% | +0.1 pts |

| Q3 2024 | 5.74% | +0.1 pts |

| Q2 2024 | 5.7% | +0.2 pts |

| Q1 2024 | 5.66% | +0.1 pts |

| Q4 2023 | 5.64% | +0.0 pts |

| Q3 2023 | 5.62% | +0.0 pts |

| Q2 2023 | 5.54% | −0.2 pts |

Frequently Asked Questions

What is the mortgage debt service ratio?

It measures mortgage payments as a percentage of household disposable personal income. In the current cycle, mortgage debt service has remained relatively contained because many homeowners locked in historically low rates during 2020–2021.

Why track mortgage debt service separately?

Mortgage and non-housing debt service have diverged in the current cycle. Low locked-in mortgage rates have kept mortgage debt service in check, while credit card and auto loan costs have surged. Tracking them separately reveals where the pressure actually is.

Where does this data come from?

The Federal Reserve publishes the mortgage debt service ratio quarterly as a component of the broader household debt service ratio. Available on FRED.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…