Total Consumer Credit Outstanding

Total consumer credit debt outstanding

What is the current Total Consumer Credit Outstanding?

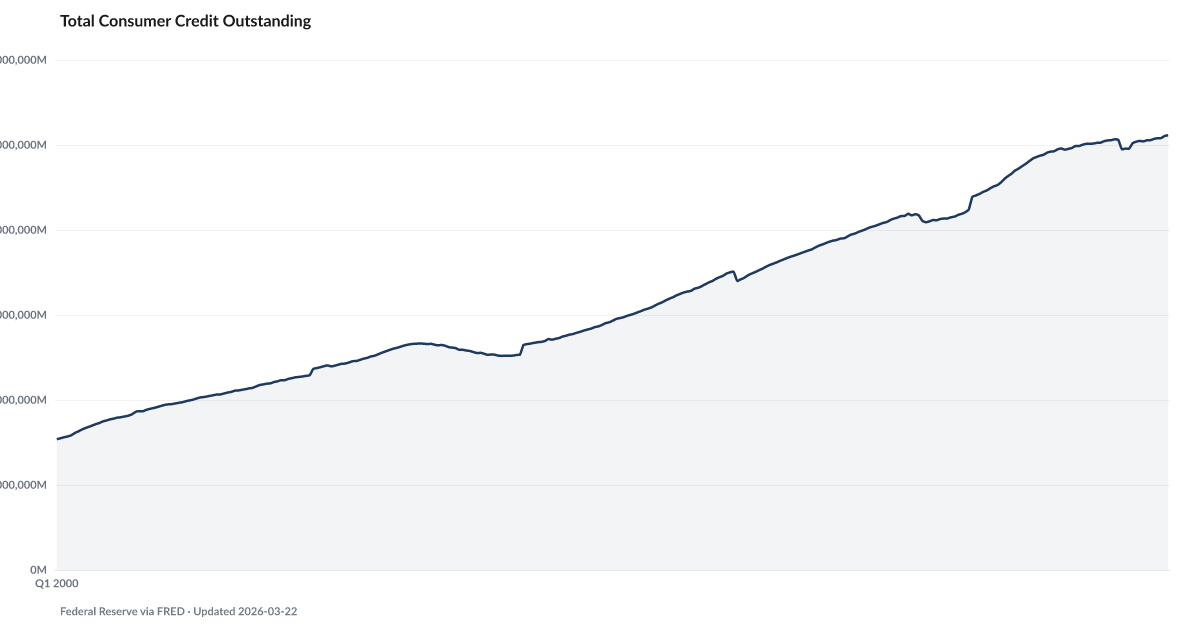

Total U.S. consumer credit outstanding — all non-mortgage consumer debt including credit cards, auto loans, student loans, and personal loans — is tracked monthly by the Federal Reserve. This aggregate figure captures the total stock of consumer borrowing, providing context for delinquency rates and debt service burden. Source: Federal Reserve G.19 Statistical Release.

Total consumer credit outstanding has climbed well above its end-of-2019 reading of $4.19 trillion, with the growth driven almost entirely by credit cards and auto loans.

The Federal Reserve's consumer credit release, FRED series TOTALSL, tracks every non-mortgage consumer loan in the United States — credit cards, auto loans, student loans, and personal loans combined. The end-of-2019 reading was $4.19 trillion. The latest reading sits hundreds of billions of dollars above that — close to a trillion dollars of additional consumer borrowing in five years.

The growth is not evenly distributed. Student loan balances have been roughly flat since the payment pause. Auto loan balances have climbed steadily as vehicle prices and interest rates both rose. Credit card balances have grown quickly, reaching new highs every quarter.

Headline debt levels, on their own, are not alarming. Nominal GDP grew over this window too. Population grew. What matters is composition and service cost. A household can carry more debt comfortably when it is secured and low-rate. Carrying it on revolving credit at over 20% APR is a different condition.

That is the shift the headline number hides. Revolving and auto debt — the most rate-sensitive, most default-prone layers — are doing most of the growth. Falling Behind picks up the stress as it surfaces. The Buffer is supposed to prevent it. With the personal savings rate near historic lows, this much consumer credit is propping up spending that household income is no longer covering on its own.

Explore Further

How has Total Consumer Credit Outstanding changed over time?

Most affected counties

Counties with the highest safety net and buffer scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| May 2026 | $5.2T | +$106.1B |

| Apr 2026 | $5.2T | +$116.1B |

| Mar 2026 | $5.1T | +$111.3B |

| Feb 2026 | $5.1T | +$152.6B |

| Jan 2026 | $5.1T | +$147.4B |

| Dec 2025 | $5.1T | +$151.3B |

| Nov 2025 | $5.1T | +$18B |

| Oct 2025 | $5.1T | +$8.9B |

| Sep 2025 | $5.1T | +$14.3B |

| Aug 2025 | $5.1T | +$3.4B |

| Jul 2025 | $5.1T | +$10.5B |

| Jun 2025 | $5T | +$17.8B |

Frequently Asked Questions

What is total consumer credit outstanding?

It is the total dollar value of all non-mortgage consumer debt in the United States, including credit card balances, auto loans, student loans, and personal installment loans. This is separate from mortgage debt, which is tracked under household debt.

Why does total consumer credit matter?

Rising consumer credit can indicate either healthy economic expansion (consumers confident enough to borrow) or distress (consumers forced to borrow to cover essential expenses). Context from delinquency rates and the savings rate helps distinguish between the two.

Where does the data come from?

The Federal Reserve publishes total consumer credit monthly in its G.19 Statistical Release. The data is broken down into revolving credit (primarily credit cards) and non-revolving credit (auto loans, student loans, personal loans).

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…