Serious Delinquency Rate (90+ days, All Loan Types)

All consumer debt 90+ days past due

What is the current Serious Delinquency Rate (90+ days, All Loan Types)?

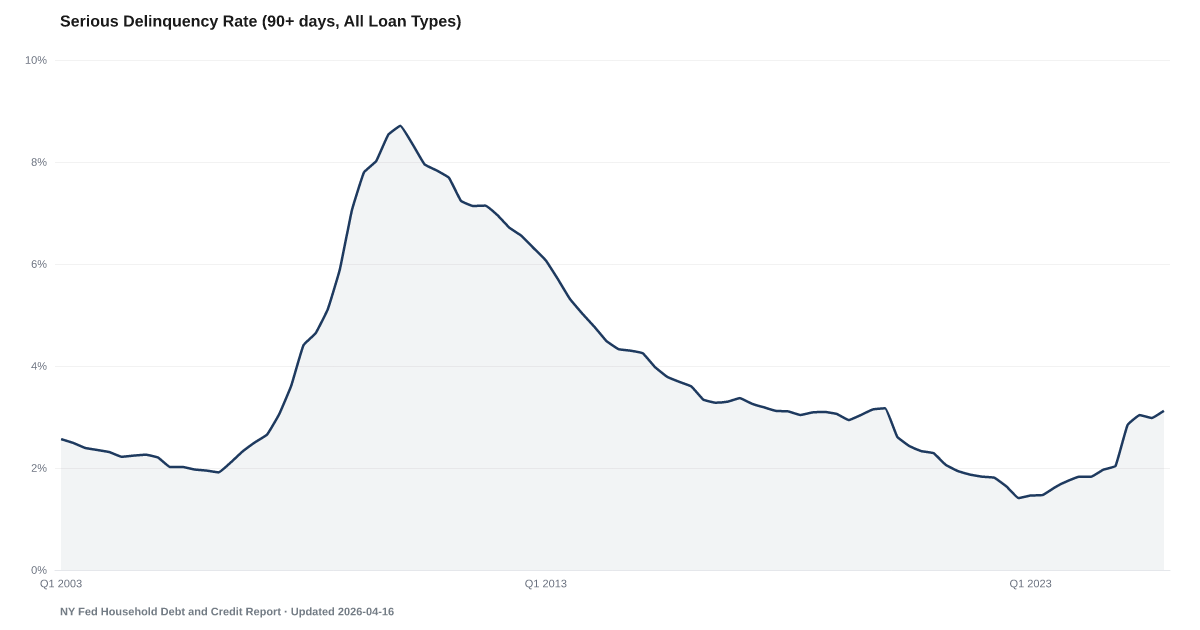

The serious delinquency rate across all consumer debt balances stood at 3.4% in Q1 2026, according to the NY Fed Consumer Credit Panel. This aggregate measure captures loans 90 or more days past due across mortgages, auto loans, credit cards, and student loans. Source: Federal Reserve Bank of New York Consumer Credit Panel.

Serious delinquency across all consumer debt has climbed to 3.4% in Q1 2026, rising in four of the last five quarters and now 138% higher than the 1.4% Q4 2022 post-stimulus low.

Ninety days behind is where temporary trouble becomes permanent damage. The credit report takes the hit. The late fees stop being recoverable. The servicer's options narrow from payment plans to legal remedies.

The NY Fed's aggregate series — which blends mortgages, credit cards, auto loans, student loans, and other consumer debt — put the 90-day rate at 3.4% in Q1 2026, rising in four of the last five quarters. The post-stimulus low was 1.4% in Q4 2022. The current reading is 138% higher than that mark. It sits in roughly the same range as Q4 2019's 3.1% — the late-cycle reading before COVID disrupted every distress series for two years.

The composition matters more than the headline. Credit Card Delinquency, Auto Loan Serious Delinquency, and Student Loan Delinquency are all elevated, with student loans jumping sharply in 2025 as reporting resumed after the payment pause. Mortgage Delinquency is the only major category not contributing.

Four straight quarters of increases have put the series back in the mid-cycle labor-market range of 2015 to 2016. The current reading is 61% below the Great Recession crest, and the labor market context is different now. Credit Card Charge-Offs are already running at an elevated post-2011 pace, which means the delinquency pipeline is converting to losses at an accelerated pace.

Explore Further

How has Serious Delinquency Rate (90+ days, All Loan Types) changed over time?

Most affected counties

Counties with the highest delinquency scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q1 2026 | 3.36% | +0.5 pts |

| Q4 2025 | 3.12% | +1.1 pts |

| Q3 2025 | 2.98% | +1.0 pts |

| Q2 2025 | 3.04% | +1.2 pts |

| Q1 2025 | 2.84% | +1.0 pts |

| Q4 2024 | 2.04% | +0.3 pts |

| Q3 2024 | 1.97% | +0.3 pts |

| Q2 2024 | 1.83% | +0.4 pts |

| Q1 2024 | 1.83% | +0.4 pts |

| Q4 2023 | 1.74% | +0.3 pts |

| Q3 2023 | 1.62% | −0.0 pts |

| Q2 2023 | 1.47% | −0.3 pts |

Frequently Asked Questions

What is the all-balance serious delinquency rate?

This rate measures the share of all consumer debt balances — mortgages, auto loans, credit cards, student loans — that are 90 or more days past due. The Q1 2026 reading is 3.4%, providing a broad view of household debt stress.

How does this differ from individual loan delinquency rates?

While individual rates show stress in specific debt categories, the all-balance rate reveals the total burden across all consumer obligations. The American Distress Index uses this as a broad debt stress signal.

Where does this data come from?

This data comes from the NY Fed Consumer Credit Panel, based on Equifax credit bureau records, published quarterly.

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…