Large vs Small Bank Credit Card Delinquency Spread

Difference between large bank and small bank credit card delinquency rates

What is the current Large vs Small Bank Credit Card Delinquency Spread?

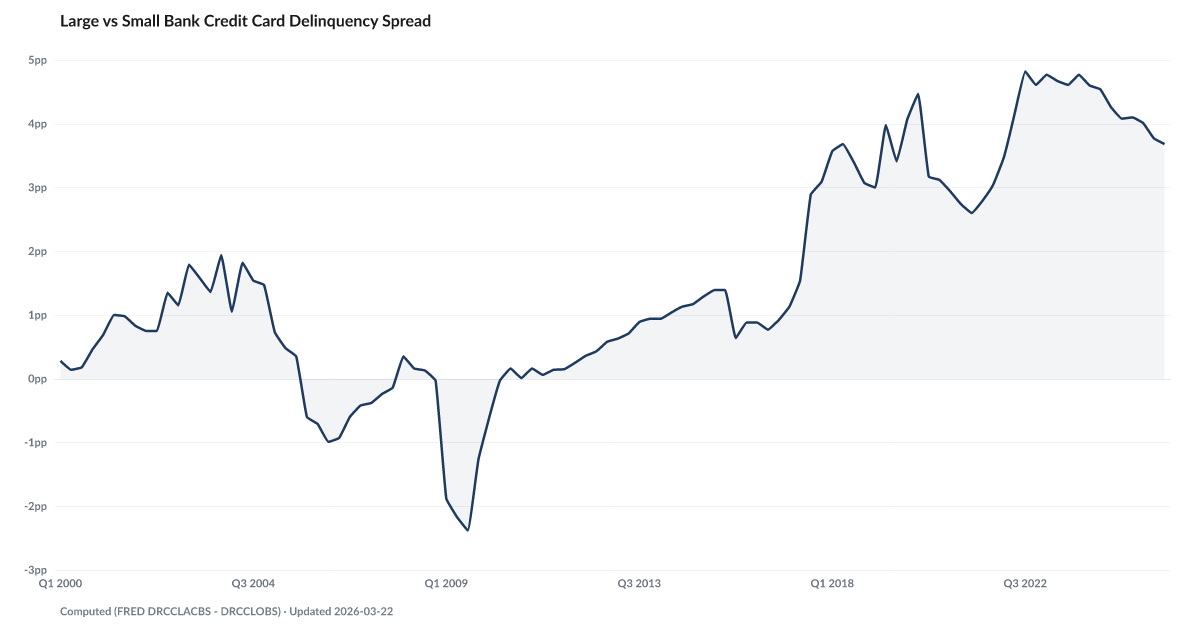

The credit card delinquency spread between large banks (top 100) and small banks reached 3.5 points in Q4 2024, with small banks reporting significantly higher default rates. This divergence signals that community and regional banks — which serve more subprime borrowers — are absorbing disproportionate credit losses. Source: FRED (DRCCLACBS, DRCCLOCBS).

Credit card delinquency at the largest U.S. banks runs 3.5 points higher than at small banks — a spread that flipped after 2015 and has stayed flipped ever since.

In the Great Recession, small banks carried more credit card distress than large banks. The spread went as negative as −2.38 percentage points in Q3 2009, when regional and community lenders bore the worst of the consumer credit losses.

That relationship reversed after 2015, and the size of the reversal is what is striking. By 2019 large banks carried roughly 4 points more delinquency than small banks. Today the spread sits at 3.5 points, down from a recent high of 4.82 in mid-2022 but still well above the pre-pandemic average.

The mechanism is the subprime book. The largest card issuers — Capital One, Discover, Synchrony, Citi — built the decade's subprime growth. Small banks mostly kept to prime borrowers. When The Risk Reset shows subprime originations climbing back toward pre-tightening levels, the loans are being written at the large banks rather than the community ones. Credit Card Charge-Offs confirm where the losses are landing.

The spread narrowing this year does not represent a return to normal. It means stress is starting to bleed into the small bank book too — the point where deteriorating labor market conditions stop being contained to the subprime segment and start showing up on balance sheets that previously looked clean.

Explore Further

Is this happening to you?

Do you bank with a smaller institution and wonder if they're under more stress?

How has Large vs Small Bank Credit Card Delinquency Spread changed over time?

Most affected counties

Counties with the highest delinquency scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q1 2026 | 3.51 pts | −0.6 pts |

| Q4 2025 | 3.66 pts | −0.4 pts |

| Q3 2025 | 3.76 pts | −0.5 pts |

| Q2 2025 | 4.02 pts | −0.5 pts |

| Q1 2025 | 4.12 pts | −0.5 pts |

| Q4 2024 | 4.06 pts | −0.7 pts |

| Q3 2024 | 4.25 pts | −0.4 pts |

| Q2 2024 | 4.55 pts | −0.1 pts |

| Q1 2024 | 4.62 pts | −0.1 pts |

| Q4 2023 | 4.76 pts | +0.1 pts |

| Q3 2023 | 4.61 pts | −0.2 pts |

| Q2 2023 | 4.68 pts | +0.5 pts |

Frequently Asked Questions

What is the large vs small bank delinquency spread?

This indicator measures the gap between credit card delinquency rates at small banks vs large banks. A wider spread indicates that smaller banks serving more vulnerable borrowers are seeing worse performance.

Why is the bank size spread important?

When small banks have much higher delinquency than large banks, it signals stress concentrated among lower-income borrowers who rely on community banks and credit unions. The American Distress Index tracks this as an early warning of broadening credit distress.

Where does this data come from?

The data comes from the Federal Reserve's quarterly charge-off and delinquency statistics, published via FRED series DRCCLACBS (large banks) and DRCCLOCBS (small banks).

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…