Auto Loan Serious Delinquency 90+ Days (NY Fed CCP)

Auto loan balances 90+ days past due, NY Fed Consumer Credit Panel

What is the current Auto Loan Serious Delinquency 90+ Days (NY Fed CCP)?

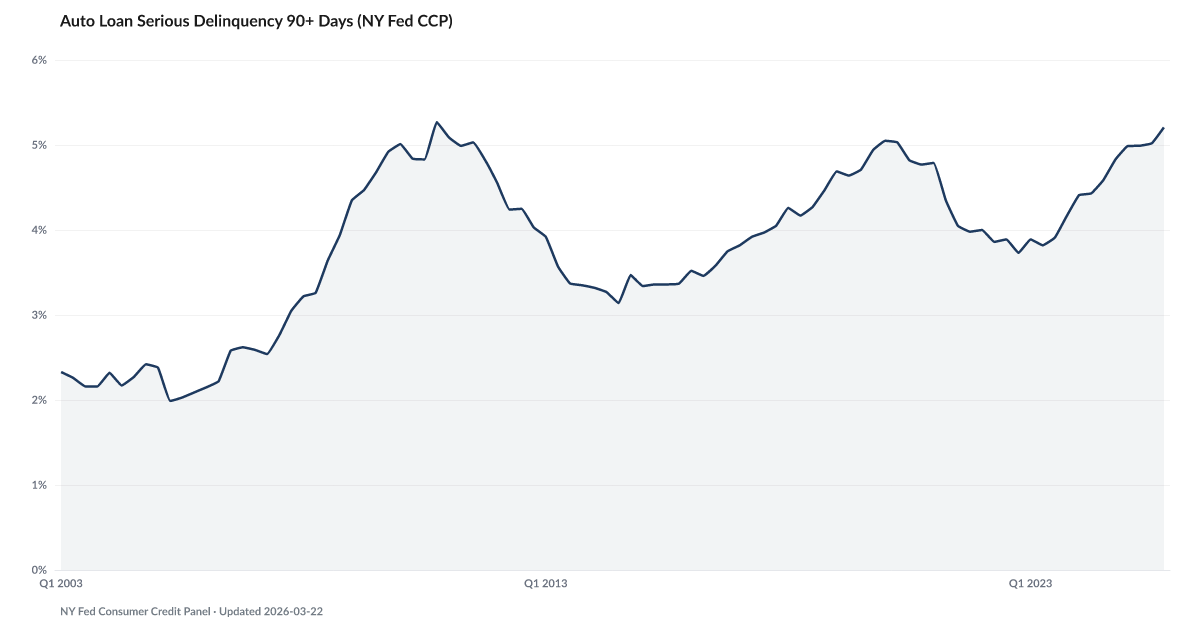

The auto loan serious delinquency rate (90+ days past due) reached 5.2% of balances in Q4 2025, according to the NY Fed Consumer Credit Panel. Auto loan delinquency is a key signal because car payments are typically prioritized over other debts — losing a vehicle means losing the ability to work for many borrowers. Source: Federal Reserve Bank of New York Consumer Credit Panel.

Auto loan serious delinquency has climbed to 5.2% in Q4 2025, roughly flat vs the Great Recession reading.

The car payment is the one most households try hardest not to miss. You can lose electricity for a weekend and survive. You cannot lose the car and get to work on Monday.

Which is what makes the latest NY Fed data notable. The share of auto loan balances 90 days or more past due reached 5.2% in Q4 2025. The series high is 5.3, set in December 2010 at the bottom of the post-GFC labor market. Today's reading is roughly flat vs that GFC-era reading.

The composition tells the harder story. Subprime borrowers, who make up roughly a fifth of the auto loan book, are driving nearly all the deterioration — their delinquency rate runs well above prime. They are the same households showing strain in Credit Card Delinquency and in The 60-Day Line, where single missed payments hardened into patterns.

Meanwhile lenders are stepping back into the credit box — The Risk Reset shows subprime originations climbing back toward their pre-tightening high. New subprime loans are being underwritten today at current rates into a weaker labor market; the current delinquency reading is roughly flat vs the Great Recession crest.

Explore Further

Is this happening to you?

Is your car payment harder to manage than when you first signed the loan?

How has Auto Loan Serious Delinquency 90+ Days (NY Fed CCP) changed over time?

Most affected counties

Counties with the highest delinquency scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q4 2025 | 5.21% | +0.4 pts |

| Q3 2025 | 5.02% | +0.4 pts |

| Q2 2025 | 4.99% | +0.6 pts |

| Q1 2025 | 4.99% | +0.6 pts |

| Q4 2024 | 4.83% | +0.7 pts |

| Q3 2024 | 4.59% | +0.7 pts |

| Q2 2024 | 4.43% | +0.6 pts |

| Q1 2024 | 4.41% | +0.5 pts |

| Q4 2023 | 4.17% | +0.4 pts |

| Q3 2023 | 3.91% | +0.0 pts |

| Q2 2023 | 3.82% | −0.0 pts |

| Q1 2023 | 3.89% | −0.1 pts |

Frequently Asked Questions

What is the auto loan serious delinquency rate?

The auto loan serious delinquency rate measures the share of auto loan balances that are 90 or more days past due. The Q4 2025 reading is 5.2%, reflecting borrowers who are at least 3 months behind on car payments.

Why are auto loan defaults important?

Auto loans are typically prioritized over other debts because losing a car means losing the ability to work. Rising auto delinquency signals severe household financial distress — borrowers have exhausted other options before letting a car loan slip.

Where does this data come from?

This data comes from the NY Fed Consumer Credit Panel, based on Equifax credit bureau records, published quarterly.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…