The Risk Reset

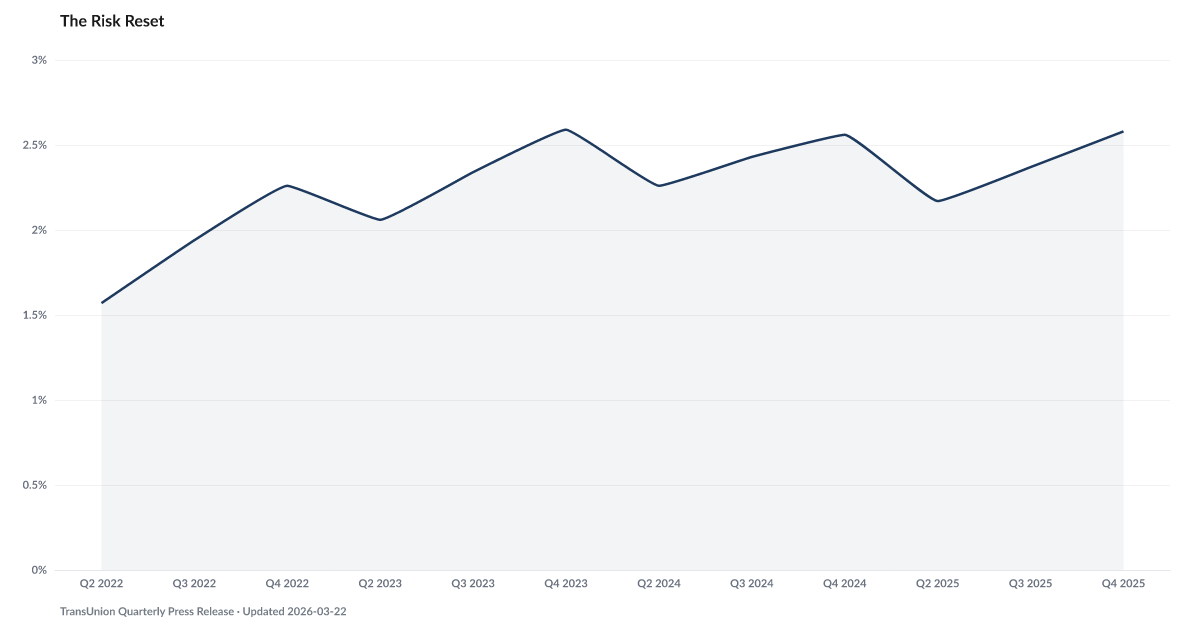

Up from 2.56% a year ago; subprime delinquency creeping back up

What is the current The Risk Reset?

TransUnion reports that subprime originations have shifted as lenders recalibrate risk appetite following pandemic-era credit expansion. This indicator tracks origination patterns among borrowers with credit scores below 620 — the segment most vulnerable to default and most sensitive to changes in lending standards. Source: TransUnion credit data.

Lenders are reopening the subprime credit box at 2.6% — higher than where it sat before the 2023 tightening cycle began.

After a bank takes losses, the standard playbook is to tighten. Subprime borrowers get cut first.

That tightening happened in 2024. Subprime originations dropped from 2.59% in Q4 2023 to 2.26% in Q2 2024 over two quarters. Then lenders watched competitors pick up the volume and started walking the reset back. TransUnion's latest reading puts the subprime share of new auto and card originations at 2.6% in Q4 2025 — essentially matching the late-2023 high, with the tightening episode written off as a brief detour.

The pattern has a history. The last time originations sat at this level heading into a weakening labor market, subprime delinquency rose 12 to 18 months later. We are watching the inputs to that cycle set up in real time, with Auto Loan Serious Delinquency already running near GFC territory.

The risk reset is really about growth. Lenders need new volume, and the bottom of the credit box is where new volume lives. The borrowers getting written into loans today are the borrowers who will fill Credit Card Charge-Off data in 2027.

Explore Further

Is this happening to you?

Has your credit score dropped recently, or do you worry it might?

How has The Risk Reset changed over time?

Most affected counties

Counties with the highest delinquency scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q4 2025 | 2.58% | +0.0 pts |

| Q3 2025 | 2.37% | −0.1 pts |

| Q2 2025 | 2.17% | −0.1 pts |

| Q4 2024 | 2.56% | −0.0 pts |

| Q3 2024 | 2.43% | +0.1 pts |

| Q2 2024 | 2.26% | +0.2 pts |

| Q4 2023 | 2.59% | +0.3 pts |

| Q3 2023 | 2.34% | +0.4 pts |

| Q2 2023 | 2.06% | +0.5 pts |

| Q4 2022 | 2.26% | — |

| Q3 2022 | 1.94% | — |

| Q2 2022 | 1.57% | — |

Frequently Asked Questions

What are subprime loan originations?

Subprime originations are new loans issued to borrowers with credit scores below 620. These borrowers pay higher interest rates and default at higher rates. Changes in subprime lending volume signal whether lenders are expanding or contracting credit access for the most vulnerable borrowers.

Why does subprime origination volume matter?

When subprime originations expand, it can indicate loosening standards that later produce delinquency waves. When they contract, it means vulnerable borrowers are being cut off from credit, potentially pushing them toward higher-cost alternatives like payday loans or Buy Now Pay Later.

Where does subprime origination data come from?

TransUnion tracks origination patterns from its consumer credit database, one of the three major credit bureaus. Data covers new account openings segmented by credit score tier, loan type, and lender size.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…