Charge-Off Rate on Credit Card Loans

Credit card debt written off as uncollectable

What is the current Charge-Off Rate on Credit Card Loans?

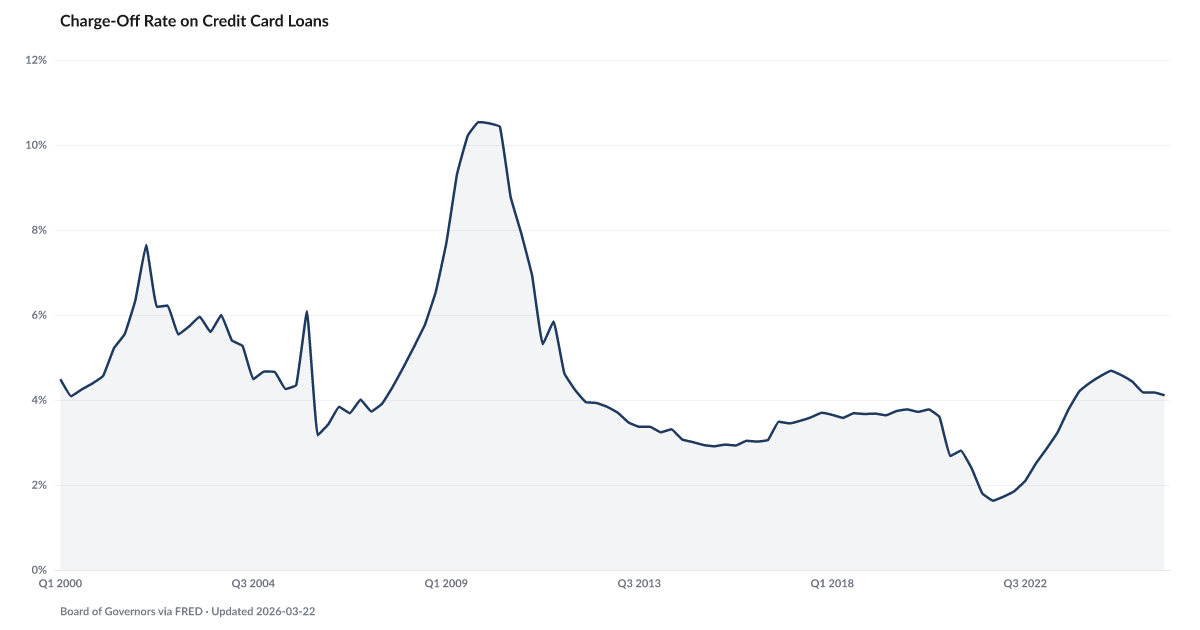

Charge-Off Rate on Credit Card Loans: 3.84% as of 2026-Q1, and improving. Source: Board of Governors via FRED (CORCCACBS).

Banks are writing off credit card debt at 3.8% — a level last sustained in 2011 and far above the 1.63% pandemic-era low.

Credit card charge-offs are the end of the line for unsecured consumer debt. The delinquency has hardened into a pattern, the collections calls have run their course, and the bank has removed the balance from its books as uncollectable.

The rate sat at 1.63% in Q4 2021 — the stimulus-era bottom, driven by stimulus payments that let households catch up on accounts that otherwise would have defaulted. By Q3 2024 it had climbed to 4.64%. It's eased since, to 3.8% in Q1 2026, but remains at a level not sustained since 2011.

The mechanics are straightforward. Credit Card Delinquency led the charge-off rate by roughly 6 to 9 months — accounts 30-60 days late today are mostly charged off inside a year if they don't cure. The 60-Day Line and the Large-Small Bank Spread both tell us where the losses are being booked: disproportionately at the largest card issuers, who built the decade's subprime growth.

Credit card charge-offs are running multiples higher than the broader All-Loan Charge-Off rate. That gap between cards and everything else is where this cycle's household distress is concentrated. Mortgage charge-offs are at zero. Corporate loan losses are contained. The credit card statement is where the damage is landing.

Explore Further

How has Charge-Off Rate on Credit Card Loans changed over time?

Most affected counties

Counties with the highest delinquency scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q1 2026 | 3.84% | −0.6 pts |

| Q4 2025 | 4.07% | −0.5 pts |

| Q3 2025 | 4.15% | −0.5 pts |

| Q2 2025 | 4.21% | −0.4 pts |

| Q1 2025 | 4.46% | +0.0 pts |

| Q4 2024 | 4.56% | +0.4 pts |

| Q3 2024 | 4.64% | +0.9 pts |

| Q2 2024 | 4.59% | +1.3 pts |

| Q1 2024 | 4.43% | +1.5 pts |

| Q4 2023 | 4.17% | +1.7 pts |

| Q3 2023 | 3.7% | +1.7 pts |

| Q2 2023 | 3.26% | +1.4 pts |

Frequently Asked Questions

What is Charge-Off Rate on Credit Card Loans?

Credit card debt written off as uncollectable

Why does Charge-Off Rate on Credit Card Loans matter for financial distress?

Charge-Off Rate on Credit Card Loans is one of the indicators tracked by the American Distress Index (ADI), which measures five dimensions of U.S. household financial distress: Delinquency, Default & Legal, Debt Burden, Labor, and Safety Net & Buffer. Changes in this indicator contribute to the overall distress picture.

Where does the Charge-Off Rate on Credit Card Loans data come from?

This data comes from Board of Governors via FRED (CORCCACBS). More information: https://fred.stlouisfed.org/series/CORCCACBS. The American Distress Index updates this indicator quarterly.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…