The 60-Day Line

Debt Stress indicator

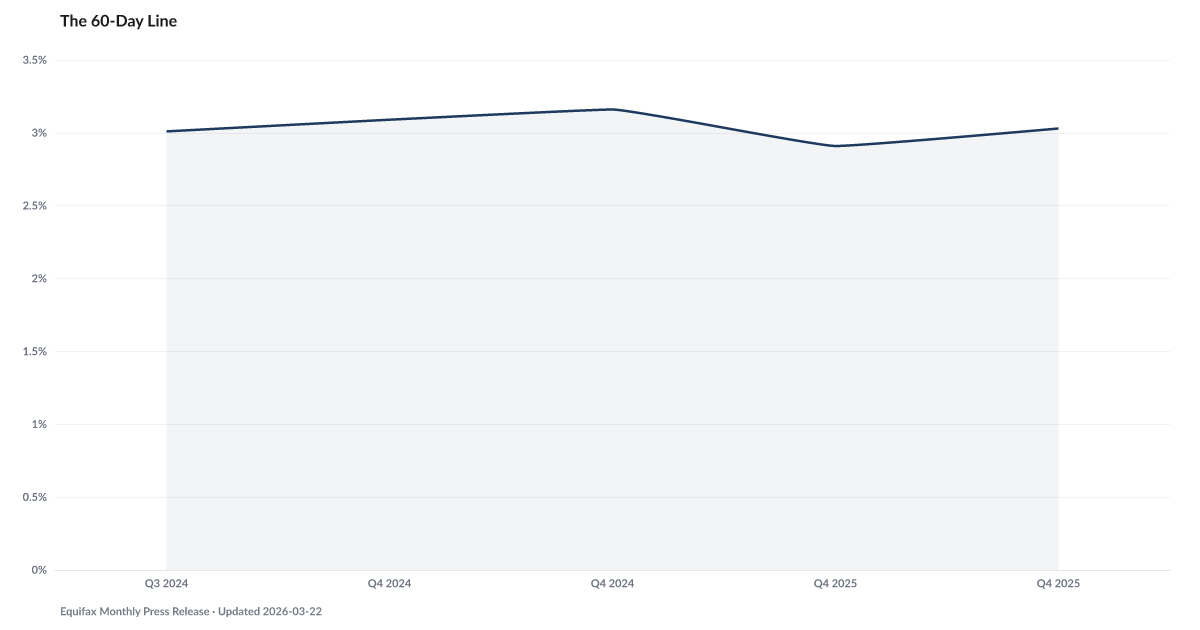

What is the current The 60-Day Line?

Equifax Monthly Credit Trends (Delinquency): 3.03% as of 2025-Q4. Source: Equifax Monthly Press Release.

Explore Further

Is this happening to you?

Have any of your accounts gone 60 or more days past due?

How has The 60-Day Line changed over time?

Most affected counties

Counties with the highest delinquency scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q4 2025 | 3.03% | −0.1 pts |

| Q4 2025 | 2.91% | −0.2 pts |

| Q4 2024 | 3.16% | — |

| Q4 2024 | 3.09% | — |

| Q3 2024 | 3.01% | — |

Frequently Asked Questions

What is Equifax Monthly Credit Trends (Delinquency)?

Debt Stress indicator

Why does Equifax Monthly Credit Trends (Delinquency) matter for financial distress?

Equifax Monthly Credit Trends (Delinquency) is one of the indicators tracked by the American Distress Index (ADI), which measures five dimensions of U.S. household financial distress: Delinquency, Default & Legal, Debt Burden, Labor, and Safety Net & Buffer. Changes in this indicator contribute to the overall distress picture.

Where does the Equifax Monthly Credit Trends (Delinquency) data come from?

This data comes from Equifax Monthly Press Release. More information: https://www.equifax.com/newsroom/. The American Distress Index updates this indicator quarterly.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…