Student Loan Delinquency Rate (90+ days)

Student loans 90+ days past due

What is the current Student Loan Delinquency Rate (90+ days)?

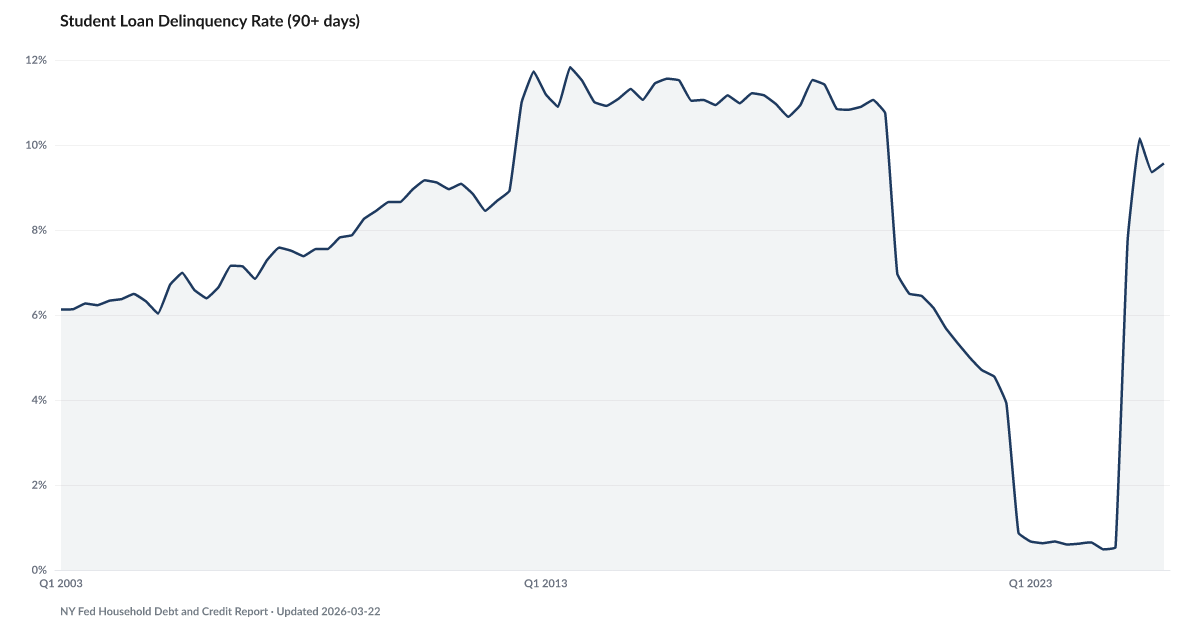

The student loan 90+ day serious delinquency rate stood at 10.3% in Q1 2026, according to the NY Fed Consumer Credit Panel. This captures borrowers at least 3 months behind on payments — a threshold that signals serious financial distress. Source: Federal Reserve Bank of New York Consumer Credit Panel.

Student loan serious delinquency jumped from 0.53% in Q4 2024 to 10.3% in Q1 2026 after the payment pause ended, returning to roughly pre-pandemic levels.

The payment pause on federal student loans lasted 42 months. When it ended, the delinquency data disappeared too — the Department of Education stopped reporting defaulted balances to credit bureaus during the on-ramp period, and the NY Fed's series flatlined near zero from Q4 2022 through Q4 2024.

Then the reporting resumed. In Q1 2025, the series jumped from 0.53% to 7.74%. By Q1 2026 it had climbed to 10.3% — nearly 1 in 10 student loan borrowers is now 90 or more days behind. Before the pandemic, the rate averaged 10 to 11%. What we're watching is post-pause distress becoming visible again in the NY Fed series.

The borrowers falling behind are disproportionately those who already owed more than they could repay. Graduates in for-profit programs. Borrowers with partial degrees and no credential. Parents who took out PLUS loans against retirement they will now need. The income-driven repayment options that were supposed to absorb the shock are caught up in litigation over the SAVE plan, which left borrowers with monthly payments they didn't expect and couldn't budget for.

Credit Card Delinquency and Auto Loan Serious Delinquency both climbed in the same quarters that student loan reporting resumed. The overlap identifies simultaneous payment stress across household balance sheets. Timing alone cannot establish that resumed student loan payments caused either increase.

Explore Further

How has Student Loan Delinquency Rate (90+ days) changed over time?

Most affected counties

Counties with the highest delinquency scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q1 2026 | 10.34% | +2.6 pts |

| Q4 2025 | 9.57% | +9.0 pts |

| Q3 2025 | 9.36% | +8.9 pts |

| Q2 2025 | 10.16% | +9.5 pts |

| Q1 2025 | 7.74% | +7.1 pts |

| Q4 2024 | 0.53% | −0.1 pts |

| Q3 2024 | 0.49% | −0.2 pts |

| Q2 2024 | 0.65% | +0.0 pts |

| Q1 2024 | 0.62% | −0.1 pts |

| Q4 2023 | 0.6% | −0.3 pts |

| Q3 2023 | 0.67% | −3.3 pts |

| Q2 2023 | 0.63% | −3.9 pts |

Frequently Asked Questions

What is the student loan serious delinquency rate?

The student loan serious delinquency rate measures the share of student loan balances that are 90 or more days past due. As of Q1 2026, 10.3% of student loan balances were seriously delinquent, according to the NY Fed.

Why does student loan delinquency matter for financial distress?

Student loan delinquency signals that borrowers are struggling to meet basic debt obligations. When combined with rising delinquency in credit cards and auto loans, it indicates broad-based household stress.

Where does the student loan delinquency data come from?

This data comes from the NY Fed Consumer Credit Panel, based on Equifax credit bureau records. It is published quarterly as part of the Quarterly Report on Household Debt and Credit.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…