Revolving Credit Utilization (75th Percentile)

Credit card utilization at the 75th percentile of active borrowers

What is the current Revolving Credit Utilization (75th Percentile)?

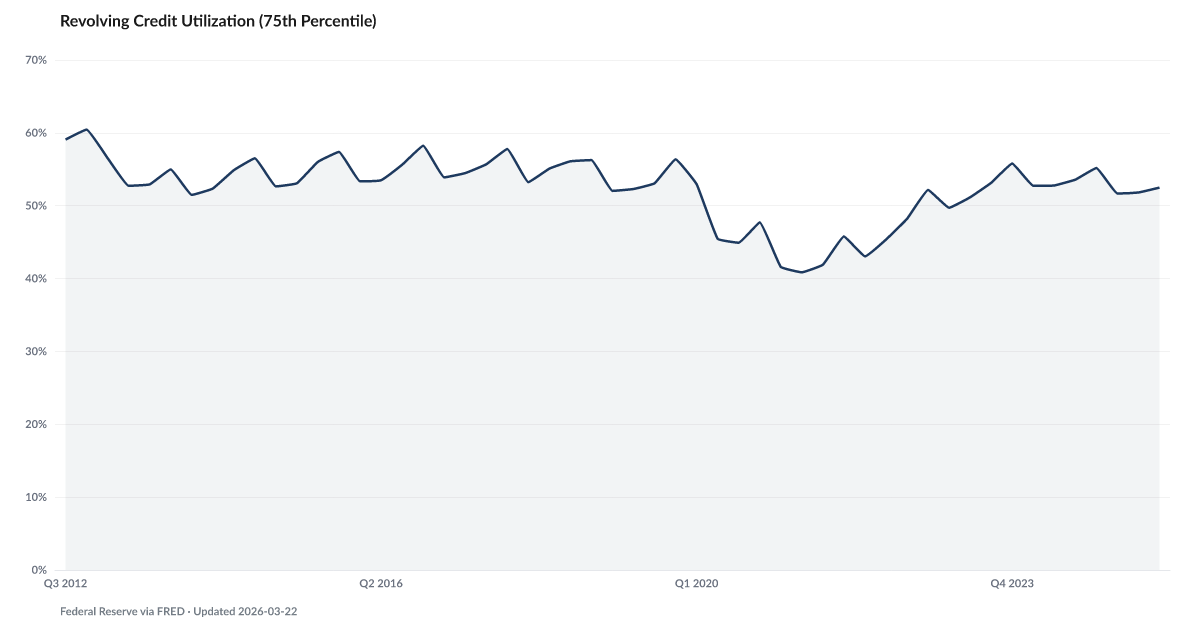

Revolving Credit Utilization (75th Percentile): 50.47% as of 2026-Q1, and improving. Source: Federal Reserve via FRED (RCCCBACTIVEUTILPCT75).

At the 75th percentile of credit card utilization, active borrowers are using 50.5% of their available credit. Well above the 30% threshold lenders treat as a warning sign.

The Federal Reserve's FRED series RCCCBACTIVEUTILPCT75 tracks credit card utilization at the 75th percentile of active borrowers. As of Q1 2026 the reading is 50.5% — well above the pandemic-era low of 40.9% (Q2 2021), and approaching the pre-pandemic range of 55 to 58%.

Thirty percent utilization is the threshold where credit scoring models start penalizing borrowers. Reading in the mid-fifties is deep into the zone where the next card offers stop coming, minimum-payment calculations climb, and the cost of being short on a bill rises sharply.

The 75th percentile is the right place to look. Median utilization numbers blend the stretched with the comfortable in a way that hides the stress. This is a direct read on the households at the edge. Their available credit — the reserve meant to absorb a car repair or an ER bill — is already being used to fund everyday life.

When utilization runs this high, the math of any new shock gets ugly fast. The Safety Net shows a minority of Americans could cover a $1,000 emergency from savings. The rest would typically reach for a credit card. At 50.5% utilization on the stressed cohort, the card is already doing most of its job. Falling Behind is the indicator that picks up what happens when the card runs out of room.

Explore Further

How has Revolving Credit Utilization (75th Percentile) changed over time?

Most affected counties

Counties with the highest safety net and buffer scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q1 2026 | 50.47% | −1.2 pts |

| Q4 2025 | 53.99% | −1.2 pts |

| Q3 2025 | 52.49% | −1.1 pts |

| Q2 2025 | 51.82% | −1.0 pts |

| Q1 2025 | 51.67% | −1.1 pts |

| Q4 2024 | 55.18% | −0.6 pts |

| Q3 2024 | 53.57% | +0.4 pts |

| Q2 2024 | 52.78% | +1.6 pts |

| Q1 2024 | 52.73% | +3.0 pts |

| Q4 2023 | 55.8% | +3.6 pts |

| Q3 2023 | 53.15% | +5.0 pts |

| Q2 2023 | 51.15% | +5.8 pts |

Frequently Asked Questions

What is Revolving Credit Utilization (75th Percentile)?

Credit card utilization at the 75th percentile of active borrowers

Why does Revolving Credit Utilization (75th Percentile) matter for financial distress?

Revolving Credit Utilization (75th Percentile) is one of the indicators tracked by the American Distress Index (ADI), which measures five dimensions of U.S. household financial distress: Delinquency, Default & Legal, Debt Burden, Labor, and Safety Net & Buffer. Changes in this indicator contribute to the overall distress picture.

Where does the Revolving Credit Utilization (75th Percentile) data come from?

This data comes from Federal Reserve via FRED (RCCCBACTIVEUTILPCT75). More information: https://fred.stlouisfed.org/series/RCCCBACTIVEUTILPCT75, https://fred.stlouisfed.org/. The American Distress Index updates this indicator quarterly.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…