Senior Loan Officer Survey: Banks Tightening Standards

Net percentage of U.S. banks tightening lending standards on consumer loans

What is the current Senior Loan Officer Survey: Banks Tightening Standards?

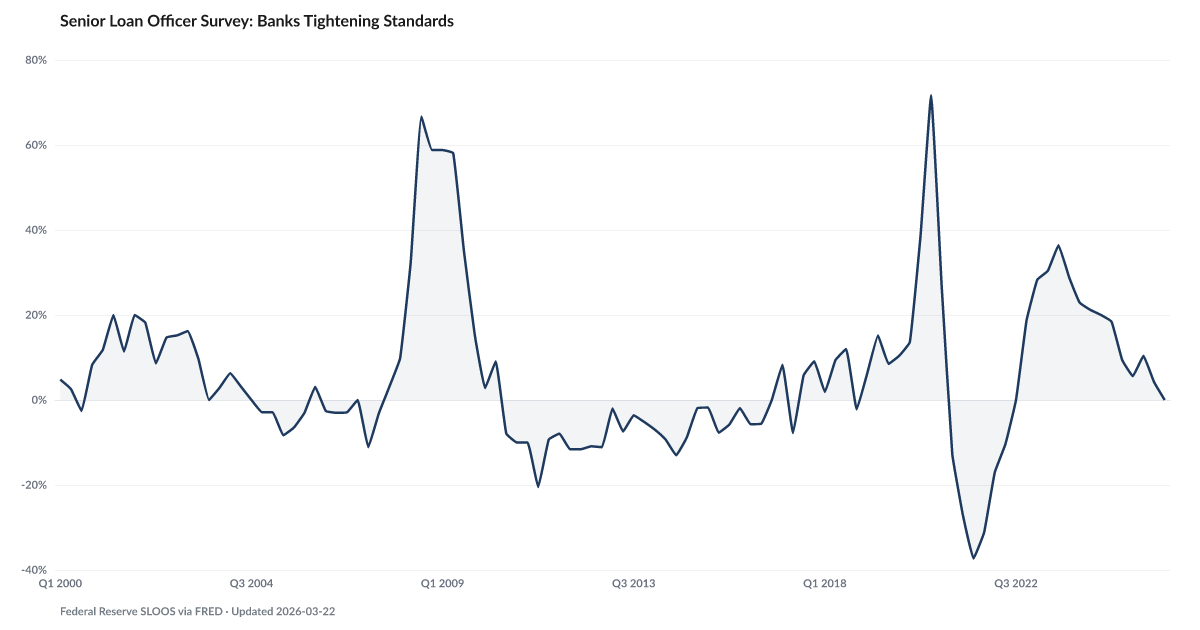

Senior Loan Officer Survey: Banks Tightening Standards: 2% as of 2026-Q2, and improving. Source: Federal Reserve SLOOS via FRED (DRTSCLCC).

The net share of U.S. banks tightening lending standards has returned to zero. That ends the longest tightening cycle in more than a decade.

The Federal Reserve's Senior Loan Officer Survey asks banks a simple question every quarter. Are you making it harder or easier to get a loan than three months ago? The answer is reported as a net percentage, the share tightening minus the share loosening. Positive means credit is harder to get. Negative means easier.

The net reading peaked above 70 percent during COVID and climbed again to roughly 36 percent in mid-2023 as the Fed hiked aggressively. It has since fallen steadily. The Q2 2026 print is zero. Banks as a group are neither tightening nor loosening. That is a meaningful inflection.

The question is what it signals. The conventional read is relief. Credit is becoming available again, which supports spending, borrowing, and the economy at the margin. The less conventional read is timing. The last two cycles, 2006-2007 and 2019, also showed net tightening rolling over to zero in the quarters just before household delinquency rates started climbing hard. Loosening doesn't cause the delinquency. It signals that banks have stopped pricing in the risk that households have already started acting on.

Falling Behind is already moving. The Late Fee confirms credit card delinquency remains elevated. The end of the tightening cycle is arriving into an environment where the underlying borrower is weaker than the headline indicators suggest. That combination has historically been where the next credit problem starts.

Explore Further

Is this happening to you?

Have you been denied credit or offered worse terms than you expected?

How has Senior Loan Officer Survey: Banks Tightening Standards changed over time?

Most affected counties

Counties with the highest debt burden scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q2 2026 | 2% | −3.6 pts |

| Q1 2026 | 0% | −9.4 pts |

| Q4 2025 | 4.2% | −14.2 pts |

| Q3 2025 | 10.4% | −9.6 pts |

| Q2 2025 | 5.6% | −15.6 pts |

| Q1 2025 | 9.4% | −13.5 pts |

| Q4 2024 | 18.4% | −10.5 pts |

| Q3 2024 | 20% | −16.4 pts |

| Q2 2024 | 21.2% | −9.2 pts |

| Q1 2024 | 22.9% | −5.4 pts |

| Q4 2023 | 28.9% | +10.1 pts |

| Q3 2023 | 36.4% | +36.4 pts |

Frequently Asked Questions

What is Senior Loan Officer Survey: Banks Tightening Standards?

Net percentage of U.S. banks tightening lending standards on consumer loans

Why does Senior Loan Officer Survey: Banks Tightening Standards matter for financial distress?

Senior Loan Officer Survey: Banks Tightening Standards is one of the indicators tracked by the American Distress Index (ADI), which measures five dimensions of U.S. household financial distress: Delinquency, Default & Legal, Debt Burden, Labor, and Safety Net & Buffer. Changes in this indicator contribute to the overall distress picture.

Where does the Senior Loan Officer Survey: Banks Tightening Standards data come from?

This data comes from Federal Reserve SLOOS via FRED (DRTSCLCC). More information: https://fred.stlouisfed.org/series/DRTSCLCC. The American Distress Index updates this indicator quarterly.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…