The FHA Signal

11.52% — up from 11.03% a year ago, government-backed loans at 6.5x the conventional rate

What is the current The FHA Signal?

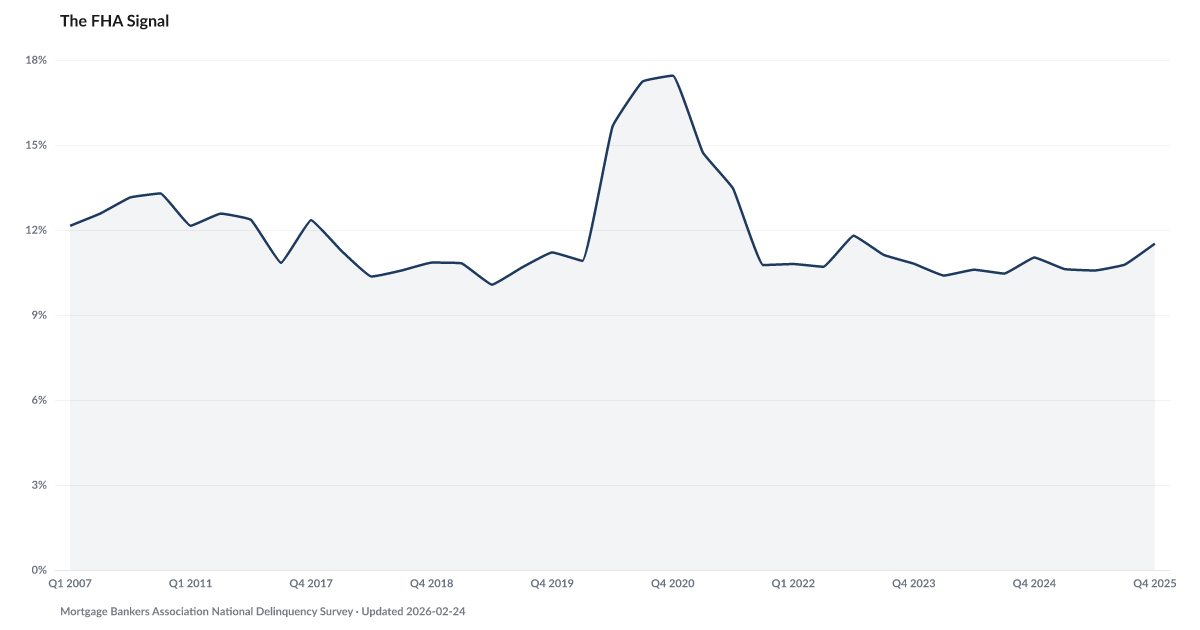

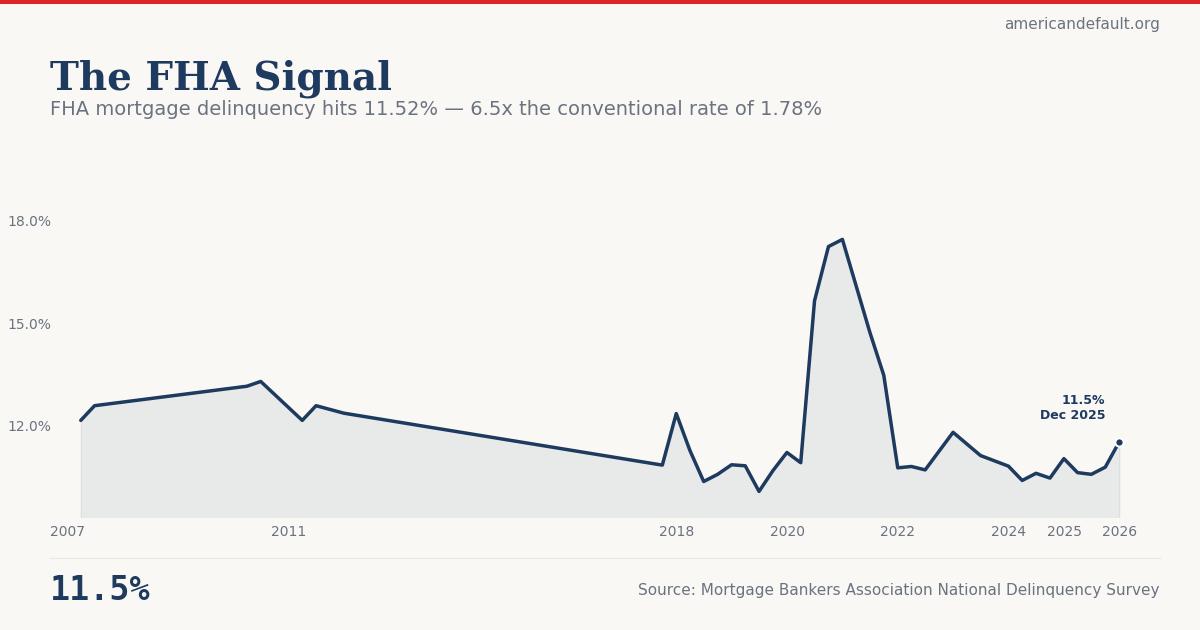

FHA delinquency rates hit 11.52% in Q4 2025, according to the Mortgage Bankers Association — nearly 6.5 times the 1.78% conventional rate and the highest level since 2021. FHA loans serve first-time buyers with thin financial cushions, making FHA delinquency a leading indicator of broader mortgage distress. The 9.74-point spread between FHA and conventional delinquency is historically unusual and signals stress concentrated among the most vulnerable borrowers. Source: MBA National Delinquency Survey (Q4 2025).

The most financially vulnerable homeowners in America are showing distress at nearly four times the rate of conventional borrowers.

FHA-insured mortgages — designed for first-time buyers and lower-income households who can't afford large down payments — showed an 11.52% delinquency rate in Q4 2025, according to the Mortgage Bankers Association's National Delinquency Survey. That is the highest reading since Q2 2021 and nearly quadruple the 2.89% conventional mortgage delinquency rate. The gap between FHA and conventional delinquency has widened to over 8 percentage points.

FHA delinquency functions as a leading indicator of broader mortgage distress because these borrowers have the thinnest financial cushions. They were the first to show strain before the 2008 crisis, too. Falling Behind tracks total delinquency across all loan types, which has risen to 4.8% — still well below crisis levels, but climbing steadily since 2021. The question is whether FHA distress stays concentrated or begins spreading into the conventional market.

The connection to broader household distress is direct. The Safety Net shows that emergency savings are at decade lows. When an FHA borrower faces an unexpected expense — a medical bill, a car repair, a temporary job loss — there's no cushion to absorb it. Missed mortgage payments become Foreclosure Filings, which have already risen 32% year-over-year.

Explore Further

Is this happening to you?

Are you struggling to keep up with your mortgage payment?

How has The FHA Signal changed over time?

{kind=link}

{kind=link}

FHA vs. Conventional Delinquency: Complete Reference Table

| Period | FHA Rate | Conventional Rate | Spread | Ratio |

|---|---|---|---|---|

| Q4 '25 | 11.52% | 1.78% | 9.74 pp | 6.5× |

| Q3 '25 | 10.78% | 1.78% | 9.00 pp | 6.1× |

| Q2 '25 | 10.57% | 1.79% | 8.78 pp | 5.9× |

| Q1 '25 | 10.62% | 1.78% | 8.84 pp | 6.0× |

| Q4 '24 | 11.03% | 1.77% | 9.26 pp | 6.2× |

| Q3 '24 | 10.46% | 1.74% | 8.72 pp | 6.0× |

| Q2 '24 | 10.60% | 1.73% | 8.87 pp | 6.1× |

| Q1 '24 | 10.39% | 1.71% | 8.68 pp | 6.1× |

| Q4 '23 | 10.81% | 1.70% | 9.11 pp | 6.4× |

| Q2 '23 | 11.12% | 1.72% | 9.40 pp | 6.5× |

| Q4 '22 | 11.80% | 1.79% | 10.01 pp | 6.6× |

| Q2 '22 | 10.70% | 1.96% | 8.74 pp | 5.5× |

| Q1 '22 | 10.80% | 2.09% | 8.71 pp | 5.2× |

| Q4 '21 | 10.76% | 2.29% | 8.47 pp | 4.7× |

| Q3 '21 | 13.47% | 2.30% | 11.17 pp | 5.9× |

| Q2 '21 | 14.73% | 2.48% | 12.25 pp | 5.9× |

| Q4 '20 | 17.45% | 2.75% | 14.70 pp | 6.3× |

| Q3 '20 | 17.24% | 2.83% | 14.41 pp | 6.1× |

| Q2 '20 | 15.65% | 2.54% | 13.11 pp | 6.2× |

| Q1 '20 | 10.91% | 2.35% | 8.56 pp | 4.6× |

| Q4 '19 | 11.21% | 2.34% | 8.87 pp | 4.8× |

| Q3 '19 | 10.68% | 2.44% | 8.24 pp | 4.4× |

| Q2 '19 | 10.07% | 2.60% | 7.47 pp | 3.9× |

| Q1 '19 | 10.82% | 2.69% | 8.13 pp | 4.0× |

| Q4 '18 | 10.85% | 2.83% | 8.02 pp | 3.8× |

| Q3 '18 | 10.57% | 2.99% | 7.58 pp | 3.5× |

| Q2 '18 | 10.36% | 3.22% | 7.14 pp | 3.2× |

| Q1 '18 | 11.27% | 3.48% | 7.79 pp | 3.2× |

| Q4 '17 | 12.35% | 3.57% | 8.78 pp | 3.5× |

| Q3 '17 | 10.84% | 3.64% | 7.20 pp | 3.0× |

| Q4 '11 | 12.36% | 10.25% | 2.11 pp | 1.2× |

| Q2 '11 | 12.58% | 10.55% | 2.03 pp | 1.2× |

| Q1 '11 | 12.15% | 10.37% | 1.78 pp | 1.2× |

| Q2 '10 | 13.29% | 11.08% | 2.21 pp | 1.2× |

| Q1 '10 | 13.15% | 11.49% | 1.66 pp | 1.1× |

| Q2 '07 | 12.58% | 2.29% | 10.29 pp | 5.5× |

| Q1 '07 | 12.15% | 2.08% | 10.07 pp | 5.8× |

Reference: What the data means

The Rate Lock Cohort Problem

FHA borrowers who originated in 2020-2022 locked in historically low rates (2.5-4.5%). They cannot refinance without paying dramatically higher rates, trapping them in homes they may no longer afford. This 'rate lock' effect means delinquent FHA borrowers cannot exit through the traditional refinance escape valve. Meanwhile, borrowers who originated in 2022-2023 at higher rates entered with minimal equity (3.5% FHA minimum), giving them the least cushion if home values stagnate.

Vintage Year Performance: 2020–2023 Originations

FHA loan performance varies dramatically by origination year. The 2020–2021 vintage locked in rates between 2.5–3.5% but entered a market where home values have since stagnated or declined in real terms. These borrowers are rate-locked but underwater on purchasing power. The 2022–2023 vintage is worse: they originated at 5.5–7.5% rates with only 3.5% down, meaning their monthly payments consume a larger share of income and they started with almost no equity cushion. HUD Neighborhood Watch data shows that loans originated in 2022–2023 are entering serious delinquency faster than any vintage since 2006–2007. The combination of high rates, minimal equity, and rising cost pressures makes these cohorts the most vulnerable in the current FHA portfolio.

Who FHA Borrowers Are

FHA mortgages serve borrowers conventional lenders often decline: first-time buyers (83% of FHA purchase loans), lower-income households, borrowers with credit scores as low as 580, and those who can only afford the 3.5% minimum down payment. The median FHA borrower income is roughly $20,000 below the conventional borrower median. When household financial stress increases, this population feels it first — and the delinquency data shows it.

From Delinquency to Foreclosure: The Pipeline

FHA delinquency is a leading indicator because it sits upstream of every other distress metric. A borrower who misses a payment enters 30-day delinquency. If they cannot catch up, they progress to 60-day, then 90+ day (serious delinquency). After 120 days, the servicer must begin loss mitigation review. If modification fails, the loan enters foreclosure — a process that takes 6-18 months depending on the state. Today's 11.52% delinquency rate is tomorrow's foreclosure pipeline.

The 2007 Parallel

In Q1 2007, FHA delinquency stood at 12.15% while conventional was just 2.08% — a 5.8x ratio. By Q1 2010, conventional had surged to 11.49%. The gap compressed from 10 points to less than 2 as the crisis spread. Today's pattern is strikingly similar: FHA at 11.52% with conventional at 1.78% — a 6.5x ratio and a 9.74-point spread. The question is whether conventional will again follow FHA upward, or whether this time the distress stays contained to the FHA population.

Why FHA Delinquency Matters for the National Picture

FHA loans represent roughly 17% of the outstanding mortgage market by count but account for a disproportionate share of delinquencies. When the MBA reports its blended national delinquency rate (currently 4.26%), FHA's 11.52% is averaged down by conventional's 1.78%. This blended number obscures a two-tier market. For policymakers and researchers, FHA delinquency functions as a stress test of the most financially vulnerable homeowners. If FHA borrowers are struggling, the households below them on the income distribution — renters, subprime cardholders, auto loan borrowers — are likely struggling more. The American Distress Index uses FHA delinquency as supporting evidence for the Debt Stress component precisely because it captures distress that blended national statistics hide.

Data Sources and Methodology

FHA delinquency data comes from the Mortgage Bankers Association (MBA) National Delinquency Survey (NDS), published quarterly. The NDS is the industry standard, covering roughly 40 million loans or about 88% of the outstanding first-lien mortgage market. FHA delinquency is defined as any FHA-insured loan that is 30 or more days past due, including loans in foreclosure. Conventional mortgage delinquency data comes from the Federal Reserve Board of Governors via FRED (series DRSFRMACBS). The spread and ratio calculations are computed by American Default from these two primary sources. Historical gaps in the FHA time series reflect quarters where MBA NDS press release data was not publicly available — the full dataset requires an MBA membership subscription.

| Period | Value | YoY Change |

|---|---|---|

| Q4 2025 | 11.52% | +0.5 pts |

| Q3 2025 | 10.78% | +0.3 pts |

| Q2 2025 | 10.57% | −0.0 pts |

| Q1 2025 | 10.62% | +0.2 pts |

| Q4 2024 | 11.03% | +0.2 pts |

| Q3 2024 | 10.46% | — |

| Q2 2024 | 10.6% | −0.5 pts |

| Q1 2024 | 10.39% | — |

| Q4 2023 | 10.81% | −1.0 pts |

| Q2 2023 | 11.12% | +0.4 pts |

| Q4 2022 | 11.8% | +1.0 pts |

| Q2 2022 | 10.7% | −4.0 pts |

Frequently Asked Questions

What is the FHA mortgage delinquency rate in 2025?

The FHA mortgage delinquency rate was 11.52% in Q4 2025, according to the Mortgage Bankers Association's National Delinquency Survey. This means roughly 1 in 9 FHA borrowers is behind on payments. The rate has risen from 10.46% in Q3 2024, with the increase accelerating in the second half of 2025.

Why is FHA delinquency so much higher than conventional mortgage delinquency?

FHA-insured mortgages serve first-time buyers and lower-income households who make smaller down payments (as low as 3.5%) and have thinner financial cushions. The median FHA borrower income is roughly $20,000 below the conventional borrower median. These borrowers are the first to show strain when costs rise or income disruption occurs. The current 6.5x gap between FHA (11.52%) and conventional (1.78%) is the widest ratio since the dataset began.

Is FHA delinquency a leading indicator of a housing crisis?

Historically, yes. In Q1 2007, FHA delinquency stood at 12.15% while conventional was just 2.08% — a 5.8x ratio. By Q1 2010, conventional had surged to 11.49% and the gap compressed to under 2 points. FHA borrowers showed stress 2-3 years before the broader market. The current 6.5x ratio (even wider than 2007) is being closely watched for the same pattern.

How does the FHA vs conventional spread compare to 2007?

The current FHA-conventional spread is 9.74 percentage points (11.52% vs 1.78%), with a 6.5x ratio. In Q1 2007, the spread was 10.07 points with a 5.8x ratio. The ratio is actually worse now. During the 2008-2010 crisis, the spread compressed to under 2 points as conventional delinquency surged to match FHA levels.

What is the rate lock problem for FHA borrowers?

FHA borrowers who originated in 2020-2022 locked in historically low rates (2.5-4.5%). They cannot refinance without paying dramatically higher rates, trapping them in homes they may no longer afford. This eliminates the traditional refinance escape valve. Meanwhile, 2022-2023 vintage borrowers entered with minimal equity (3.5% FHA minimum down payment), giving them the least cushion if home values stagnate.

How does FHA delinquency connect to foreclosures?

Delinquent FHA loans feed directly into the foreclosure pipeline. After 120 days of delinquency, servicers must begin loss mitigation review. If modification fails, the loan enters foreclosure — a process taking 6-18 months depending on the state. Today's 11.52% delinquency rate is tomorrow's foreclosure inventory. Foreclosure filings have already risen 32% year-over-year.

Who are FHA borrowers?

About 83% of FHA purchase loans go to first-time homebuyers. FHA borrowers typically have credit scores as low as 580, make the minimum 3.5% down payment, and earn roughly $20,000 less per year than conventional borrowers. FHA mortgages are designed to expand homeownership access — but that means FHA borrowers have the thinnest financial margins and are most exposed to economic stress.

Where does FHA delinquency data come from?

The primary source is the Mortgage Bankers Association's quarterly National Delinquency Survey, the industry benchmark for mortgage performance data. Supplementary monthly data comes from HUD's Single-Family Loan Performance Trends reports. The American Distress Index tracks both sources to monitor FHA delinquency as a leading indicator of household financial distress.

What should I do if I'm behind on my FHA mortgage?

Contact your servicer immediately — FHA loans have special loss mitigation options including FHA-HAMP modifications, partial claims, and forbearance. Call HUD's free housing counselor hotline at 1-800-569-4287 for expert guidance. Acting early gives you the most options. See our foreclosure prevention guide at americandefault.org/help/foreclosure/stop-foreclosure/ for step-by-step instructions.

Which FHA loan vintages are performing worst?

Loans originated in 2022-2023 are entering serious delinquency faster than any vintage since 2006-2007, according to HUD Neighborhood Watch data. These borrowers originated at 5.5-7.5% rates with only 3.5% down payment, meaning high monthly payments and minimal equity cushion. The 2020-2021 vintage has a different problem: borrowers locked in low rates (2.5-3.5%) but are now rate-locked, unable to refinance their way out of financial difficulty.

What is the national blended mortgage delinquency rate and why is it misleading?

The MBA's blended national delinquency rate is 4.26% as of Q4 2025. This combines FHA (11.52%), VA, and conventional (1.78%) loans into a single number. The blended rate obscures a two-tier mortgage market: conventional borrowers are performing near historical bests while FHA borrowers are experiencing stress levels comparable to the pre-crisis period. The American Distress Index tracks FHA separately to reveal distress that aggregate statistics hide.

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…