The Safety Net

41% — down from 44% a year ago; the rest borrow or skip it

What is the current The Safety Net?

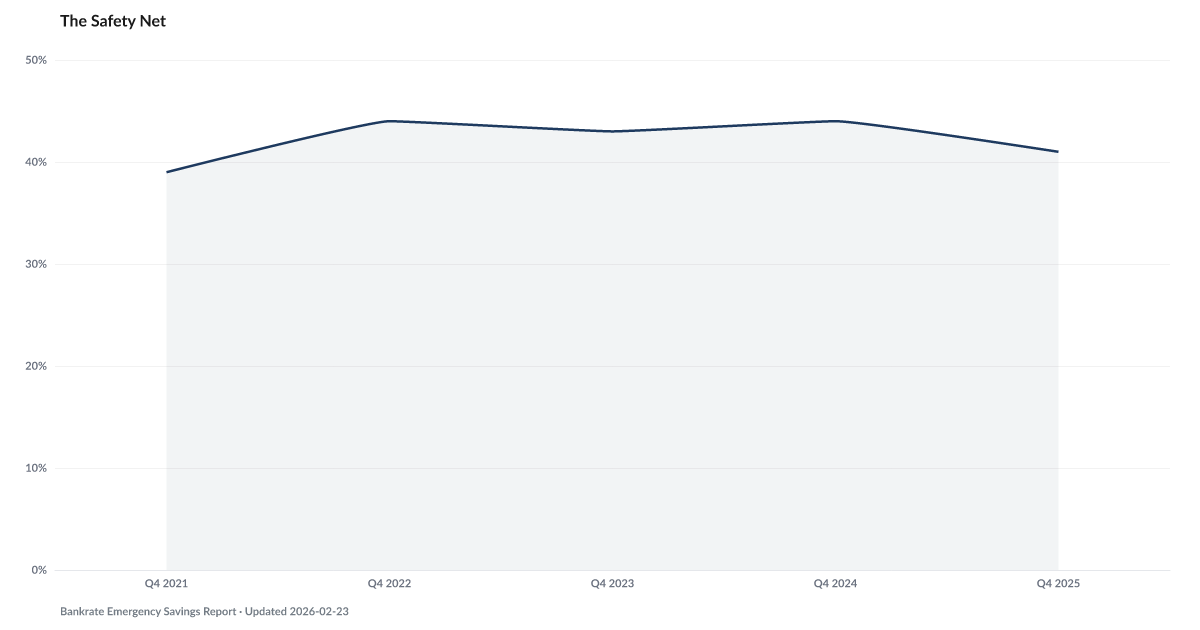

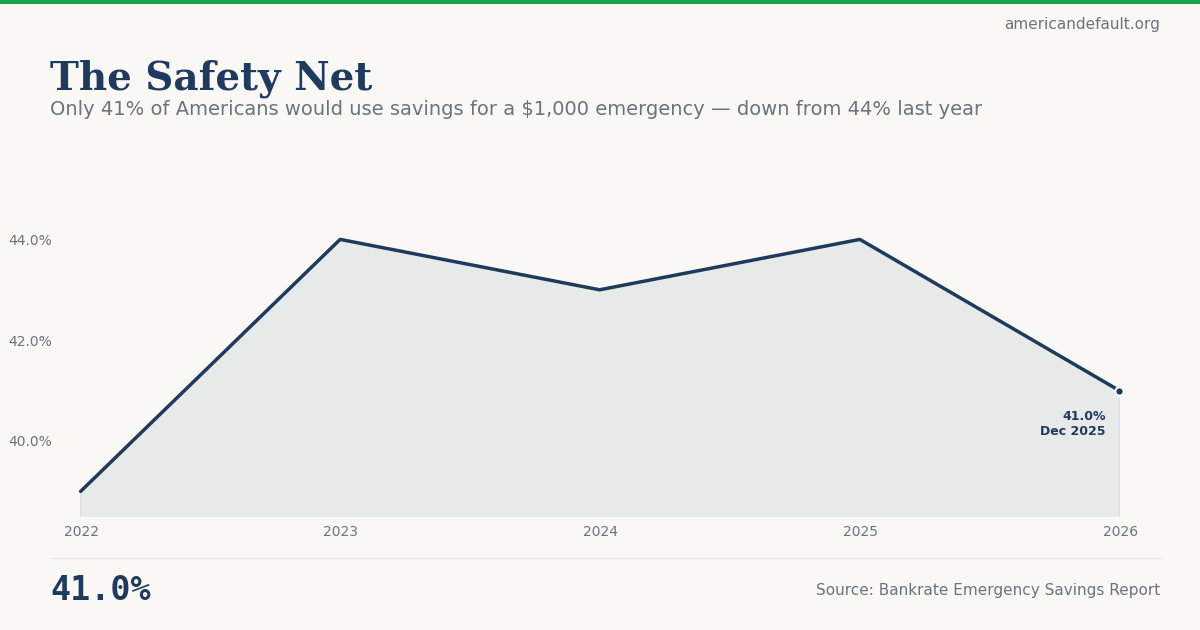

Only 41% of Americans could pay for a $1,000 emergency expense from savings in 2024, according to Bankrate's annual Emergency Savings Report — down 3 percentage points from the prior year and the weakest reading since the survey began. Meanwhile, 27% of Americans reported having no emergency savings at all, the highest share since the pandemic year of 2020. Source: Bankrate Emergency Savings Report (January 2025).

The share of Americans who could handle a surprise $1,000 expense using savings alone has fallen to its lowest point in a decade.

Bankrate’s annual Emergency Savings Report, based on a survey of 1,052 adults conducted in December 2024 and published January 2025, found that just 41% of Americans could pay for a $1,000 emergency from savings — down 3 percentage points from the prior year and the weakest reading since the survey began.

Meanwhile, the share of Americans with no emergency savings at all climbed to 27%, the highest since the pandemic year of 2020. Among those who do have savings, the amounts are thin: the median emergency fund sits at roughly $500, insufficient to cover even a modest car repair or medical bill.

This erosion isn’t happening in isolation. The Cannibalization Rate shows 401(k) hardship withdrawals up 365% from pre-pandemic levels — Americans are eating their retirement to survive today. The Buffer confirms it from the macro side: the personal savings rate has dropped to 3.5%, near historic lows. And The Squeeze shows 24% of households now spend 95% or more of their income on necessities, leaving almost nothing to rebuild reserves.

In previous cycles, this pattern — thinning savings, rising hardship withdrawals, collapsing personal savings rate — preceded spikes in delinquency and default by 6 to 9 quarters. The buffer erodes first. The defaults come later.

Explore Further

Is this happening to you?

Could you cover a $1,000 emergency without borrowing?

How has The Safety Net changed over time?

{kind=link}

{kind=link}

| Period | Value | YoY Change |

|---|---|---|

| 2025 | 41% | −3.0 pts |

| 2024 | 44% | +1.0 pts |

| 2023 | 43% | −1.0 pts |

| 2022 | 44% | +5.0 pts |

| 2021 | 39% | — |

Frequently Asked Questions

What percentage of Americans could handle a $1,000 emergency?

As of the 2024 Bankrate survey (published January 2025), only 41% of Americans could pay for a $1,000 emergency expense using savings alone. This is down 3 percentage points from the prior year and the lowest reading since Bankrate began tracking this question.

How many Americans have no emergency savings at all?

27% of Americans reported having no emergency savings at all in the 2024 Bankrate survey, the highest share since 2020. Among those who do have savings, the median emergency fund sits at roughly $500 — insufficient to cover even a modest car repair or medical bill.

Is the emergency savings situation getting better or worse?

It is worsening. The share of Americans who could cover a $1,000 emergency from savings has fallen from a peak following pandemic stimulus payments to 41% in 2024, the lowest in a decade. The share with zero savings has risen to 27%. Multiple data sources — including the Fed's SHED survey and the personal savings rate — confirm the same downward trend.

How does emergency savings relate to loan defaults?

Depleted emergency savings are a leading indicator of future loan defaults. When households lack financial buffers, any unexpected expense — a medical bill, car repair, or job loss — can trigger missed payments. American Distress Index analysis shows that buffer depletion precedes debt stress by approximately 9 quarters.

Where does the emergency savings data come from?

This indicator uses Bankrate's annual Emergency Savings Report, based on a nationally representative survey of over 1,000 adults conducted in December 2024 and published January 2025. The American Distress Index cross-references this with the Fed's SHED survey ($400 Test) for confirmation.

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…