Foreclosure Filings

32.0% — up from 9% a year ago, with no sign of the surge reversing

What is the current Foreclosure Filings?

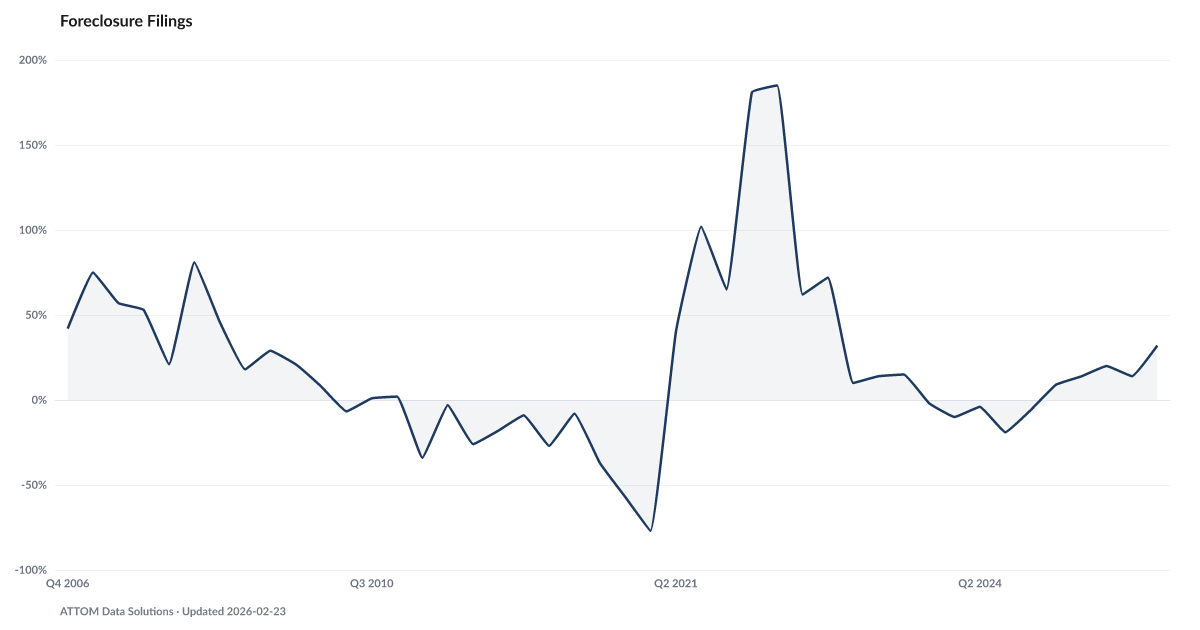

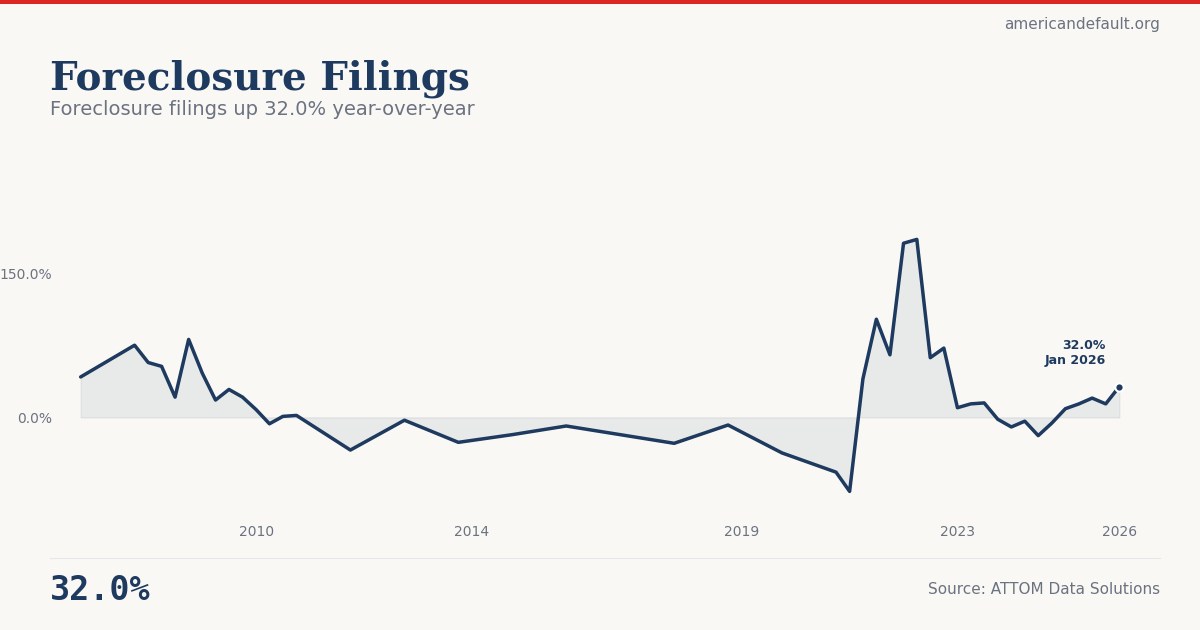

Foreclosure filings rose 32% year-over-year in Q1 2026, according to ATTOM Data Solutions — the strongest quarterly increase since the post-moratorium rebound of 2022. This follows three consecutive quarters of rising filings after a period of declines, marking a clear trend reversal from the near-zero pandemic-era floor. The pipeline from FHA delinquency (11.52%) through formal proceedings is now active and accelerating. Source: ATTOM Data Solutions (Q1 2026).

After years of pandemic-era suppression, foreclosure activity has turned decisively upward.

Foreclosure filings rose 32% year-over-year in Q1 2026, according to ATTOM Data Solutions — the strongest quarterly increase since the post-moratorium rebound of 2022. This follows three consecutive quarters of rising filings after a period of declines, marking a clear trend reversal. The pandemic-era moratoriums and historically low mortgage rates had pushed foreclosure activity to near-zero; that floor has now given way.

The pipeline from mortgage distress to foreclosure is visible in The FHA Signal, which shows FHA delinquency at 11.52% — the highest since 2021. FHA borrowers, who typically have smaller equity cushions and fewer financial reserves, are the first to transition from delinquency to formal proceedings. As these filings convert to completed foreclosures, they appear in housing inventory data and neighborhood price effects over the following 12–18 months.

The current level is still far below the crisis peak, when foreclosure filings were running 80–180% above prior years. But the direction matters more than the magnitude at this stage. Bankruptcy Filings are up 20% year-over-year, and The Wipeout Ratio shows Chapter 7 liquidations outpacing Chapter 13 reorganizations at the widest margin since 2022. When families choose total liquidation over restructuring, it suggests the financial damage is too deep to reorganize around.

Explore Further

Is this happening to you?

Have you received any notices from your mortgage servicer that worried you?

How has Foreclosure Filings changed over time?

{kind=link}

{kind=link}

| Period | Value | YoY Change |

|---|---|---|

| Q1 2026 | 32% | +23.0 pts |

| Q4 2025 | 14% | +20.0 pts |

| Q3 2025 | 20% | +39.0 pts |

| Q2 2025 | 13.9% | +17.9 pts |

| Q1 2025 | 9% | +19.0 pts |

| Q4 2024 | -6% | −4.0 pts |

| Q3 2024 | -19% | −34.0 pts |

| Q2 2024 | -4% | −18.0 pts |

| Q1 2024 | -10% | −20.0 pts |

| Q4 2023 | -2% | −74.0 pts |

| Q3 2023 | 15% | −47.0 pts |

| Q2 2023 | 14% | −171.0 pts |

Frequently Asked Questions

How much have foreclosure filings increased?

Foreclosure filings rose 32% year-over-year in Q1 2026, according to ATTOM Data Solutions. This follows three consecutive quarters of rising filings, marking a clear trend reversal from the pandemic-era suppression that pushed foreclosure activity to near zero.

Is the U.S. heading for another foreclosure crisis like 2008?

Current levels remain far below crisis peaks, when filings were running 80–180% above prior years. However, the direction of the trend matters more than the absolute level at this early stage. The pipeline from FHA delinquency (11.52%) through formal proceedings is active, and the transition from delinquency to completed foreclosure typically takes 12–18 months.

Which borrowers are most at risk of foreclosure?

FHA borrowers show the most distress, with an 11.52% delinquency rate — nearly four times the conventional rate. FHA borrowers typically have smaller equity cushions and fewer financial reserves, making them the first to transition from delinquency to foreclosure.

How long does the foreclosure process take?

The timeline varies by state. In non-judicial foreclosure states like California and Texas, it can take as little as 120 days. In judicial states like New York and New Jersey, the process can take a year or more. As filings convert to completed foreclosures, they appear in housing inventory and neighborhood price data over the following 12–18 months.

Where does foreclosure filing data come from?

ATTOM Data Solutions tracks foreclosure filings from county recorder offices nationwide, including default notices, scheduled auctions, and bank repossessions. Data is published quarterly and includes year-over-year comparisons.

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…