The Tightening

Chicago Fed measure of non-financial leverage conditions

What is the current The Tightening?

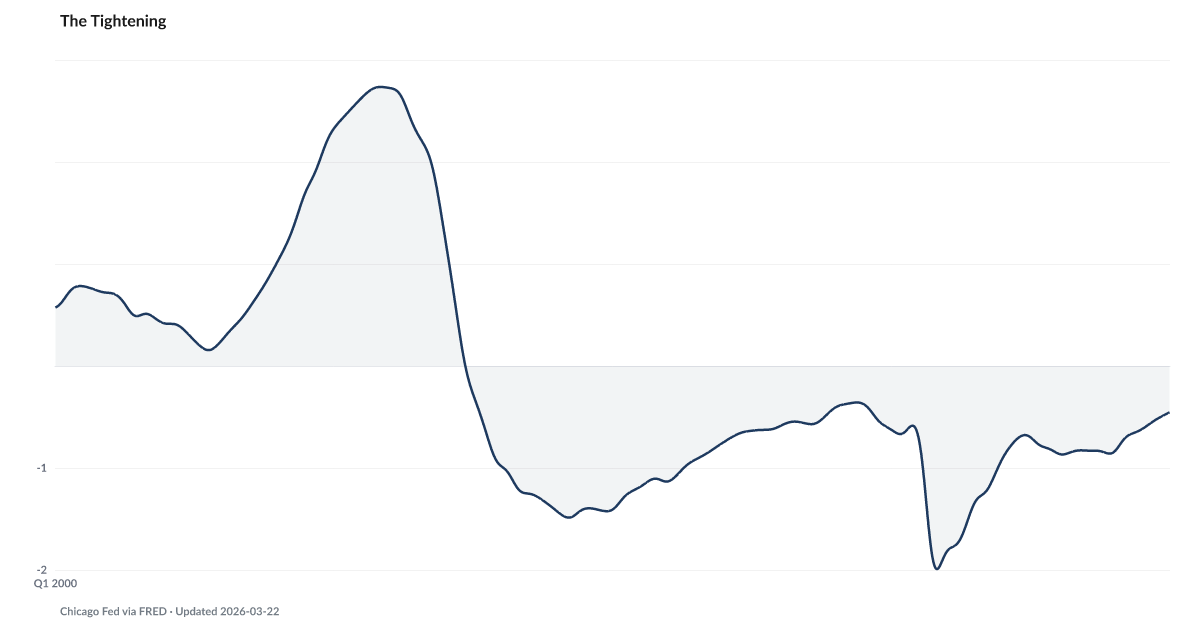

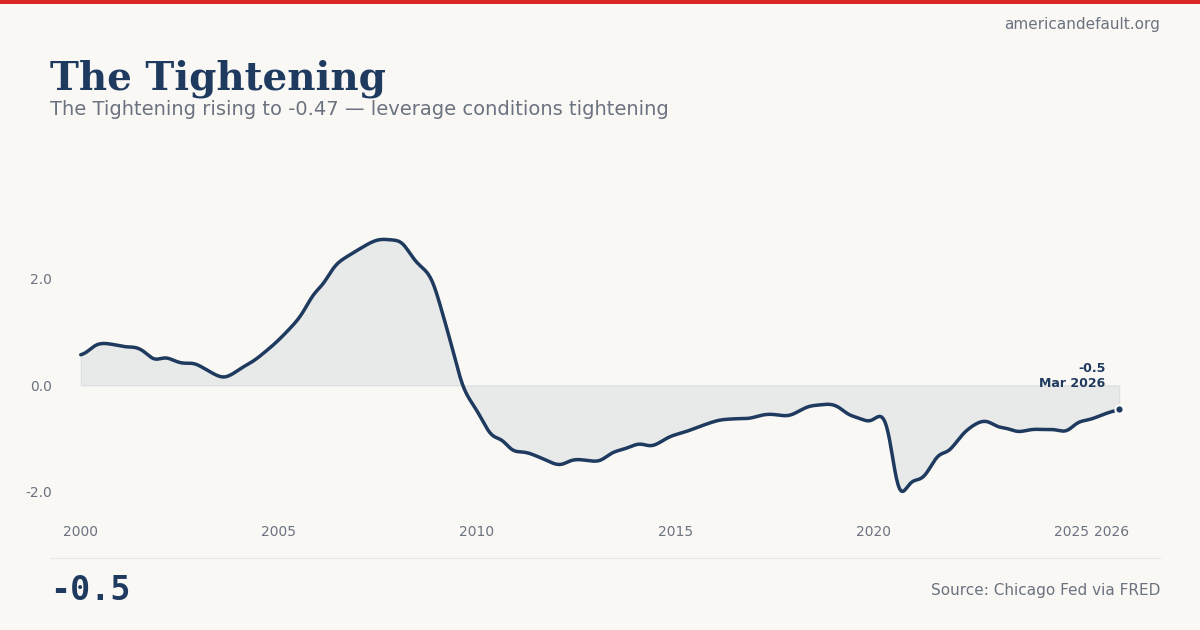

The Chicago Fed's NFCI Non-Financial Leverage Subindex stood at -0.47 in February 2026, up from -0.86 in late 2023 — the fastest tightening pace since the post-pandemic normalization. In this index, zero represents average historical conditions and positive values indicate tighter-than-average leverage. While still technically in loose territory, the speed and direction of the move signal that borrowing is becoming harder and more expensive across the economy. Source: Chicago Fed (February 2026).

Financial leverage conditions are tightening at the fastest pace in years, moving steadily toward levels that have historically preceded credit stress.

The Chicago Fed's NFCI Non-Financial Leverage Subindex stood at -0.47 in February 2026, up from -0.86 in late 2023. In this index, zero represents average historical conditions and positive values indicate tighter-than-average leverage. The current reading is still negative — meaning conditions are technically looser than the historical average — but the speed and direction of the move matters more than the absolute level. The index has risen nearly 0.4 points since its recent trough, the fastest tightening pace since the post-pandemic normalization.

Leverage tightening means that borrowing is becoming harder and more expensive across the economy. This confirms what individual indicators already show: The Card Tax at a record 20.97% APR, The Warning Light below its recession threshold for 13 months, and The Mood Ring at levels not seen outside of recessions. The NFCI provides a single composite measure that integrates dozens of market-based signals into one directional reading.

In the pre-GFC period, this index rose from roughly -0.9 in 2003 to +2.7 in 2007, spending years above zero before the crisis hit. In the current cycle, it's rising from -0.86 but has not yet crossed zero. Debt Service at 11.3% of disposable income suggests that households are already feeling the effects of tighter conditions even before the index reaches its stress threshold.

Explore Further

Is this happening to you?

Have you noticed higher interest rates or tighter credit terms on your accounts?

How has The Tightening changed over time?

{kind=link}

{kind=link}

| Period | Value | YoY Change |

|---|---|---|

| Mar 2026 | -0.45 | +0.23 |

| Mar 2026 | -0.46 | +0.24 |

| Feb 2026 | -0.46 | +0.24 |

| Feb 2026 | -0.47 | +0.24 |

| Feb 2026 | -0.47 | +0.25 |

| Feb 2026 | -0.47 | +0.25 |

| Jan 2026 | -0.48 | +0.26 |

| Jan 2026 | -0.48 | +0.27 |

| Jan 2026 | -0.49 | +0.27 |

| Jan 2026 | -0.49 | +0.28 |

| Jan 2026 | -0.5 | +0.29 |

| Dec 2025 | -0.5 | +0.30 |

Frequently Asked Questions

What does the NFCI leverage subindex measure?

The Chicago Fed's National Financial Conditions Index (NFCI) leverage subindex measures non-financial sector leverage conditions. Zero represents average historical conditions, negative values indicate looser-than-average conditions, and positive values indicate tighter-than-average conditions.

Are financial conditions tightening?

Yes. The index has risen from -0.86 in late 2023 to -0.47 in February 2026 — a nearly 0.4-point move representing the fastest tightening pace since the post-pandemic normalization. While still technically in loose territory, the direction and speed of the move signal that credit is becoming more expensive and harder to access.

How does the current reading compare to the 2008 crisis?

In the pre-2008 period, this index rose from roughly -0.9 in 2003 to +2.7 in 2007, spending years above zero before the crisis. The current index at -0.47 has not yet crossed zero but is moving in that direction at an accelerating pace.

What does tightening mean for households?

Tightening leverage conditions mean that borrowing becomes harder and more expensive. This is already visible in individual indicators: credit card APRs at a record 20.97%, rising delinquency across loan types, and household debt service consuming 11.3% of disposable income.

Where does the NFCI data come from?

The Chicago Fed publishes the National Financial Conditions Index weekly, incorporating over 100 measures of financial activity across money markets, debt markets, equity markets, and the banking system. The leverage subindex specifically tracks non-financial sector borrowing conditions.

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…