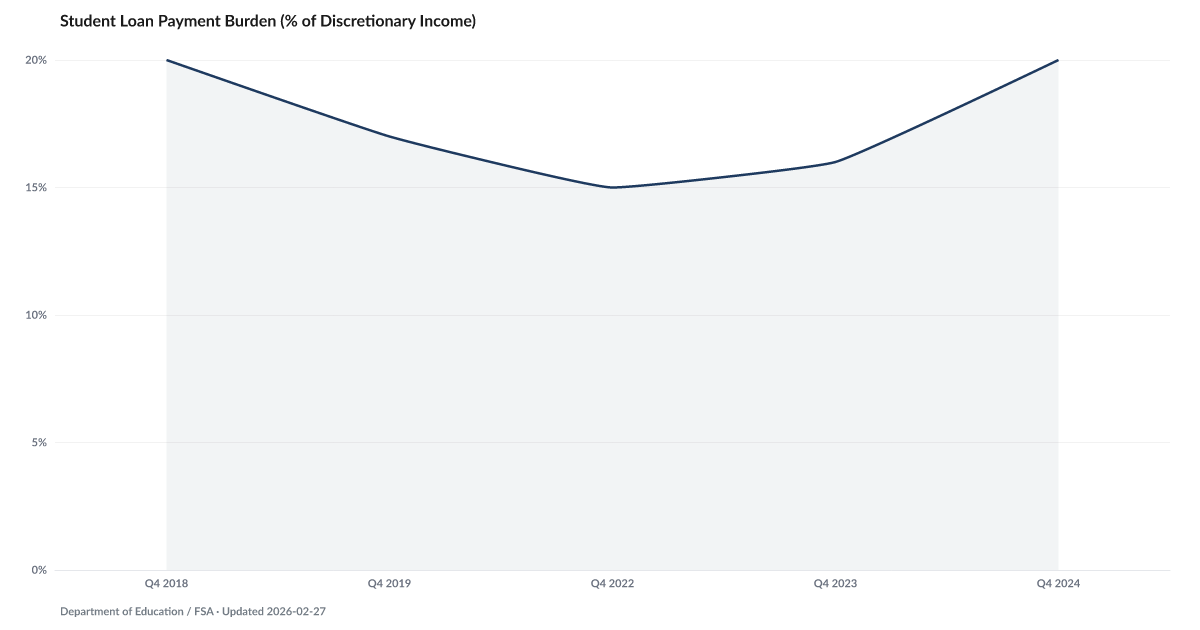

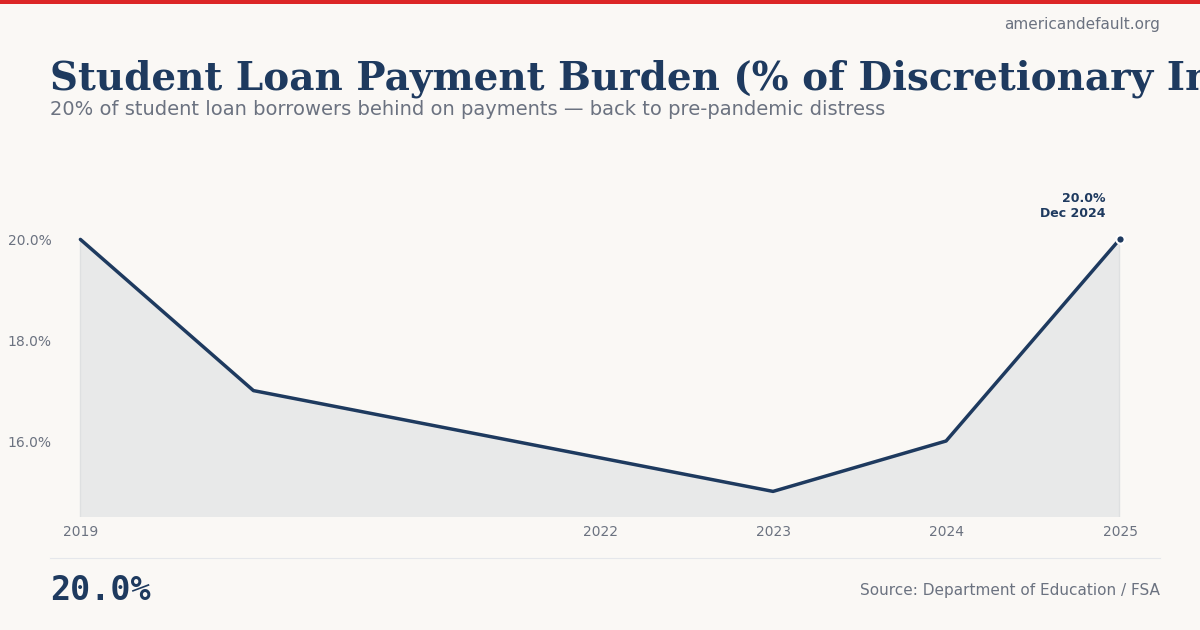

Student Loan Payment Burden (% of Discretionary Income)

20.0% — up from 16.0% a year ago, one of every five dollars earned

What is the current Student Loan Payment Burden (% of Discretionary Income)?

Student loan borrowers are spending approximately 20% of their discretionary income on loan payments — one of every five dollars earned after taxes and necessities goes to student debt service. This burden increased sharply after the expiration of the pandemic-era payment pause, which had temporarily reduced required payments to zero for federal borrowers. Source: Federal Reserve / BLS analysis.

20% of student loan borrowers behind on payments — back to pre-pandemic distress

Payment pause masked distress 2020-2022. First full post-restart year matches 2018 levels.

Explore Further

How has Student Loan Payment Burden (% of Discretionary Income) changed over time?

{kind=link}

{kind=link}

| Period | Value | YoY Change |

|---|---|---|

| 2024 | 20% | +4.0 pts |

| 2023 | 16% | +1.0 pts |

| 2022 | 15% | — |

| 2019 | 17% | −3.0 pts |

| 2018 | 20% | — |

Frequently Asked Questions

How much income do student loan borrowers spend on payments?

Student loan borrowers spend approximately 20% of their discretionary income on loan payments. For many borrowers — particularly those with graduate school debt or those earning modest incomes — this effectively eliminates the ability to save, invest, or build a financial cushion.

What happened when student loan payments resumed?

The pandemic-era payment pause, which ran from March 2020 through late 2024, temporarily reduced required federal student loan payments to zero. When payments resumed, borrowers who had spent three years without this obligation suddenly faced hundreds of dollars in monthly payments, compressing already-tight budgets.

Where does student loan burden data come from?

Student loan payment burden estimates draw from Federal Reserve consumer credit data, the SHED survey, and BLS income data. The American Distress Index tracks the ratio of required student loan payments to borrower discretionary income.

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…