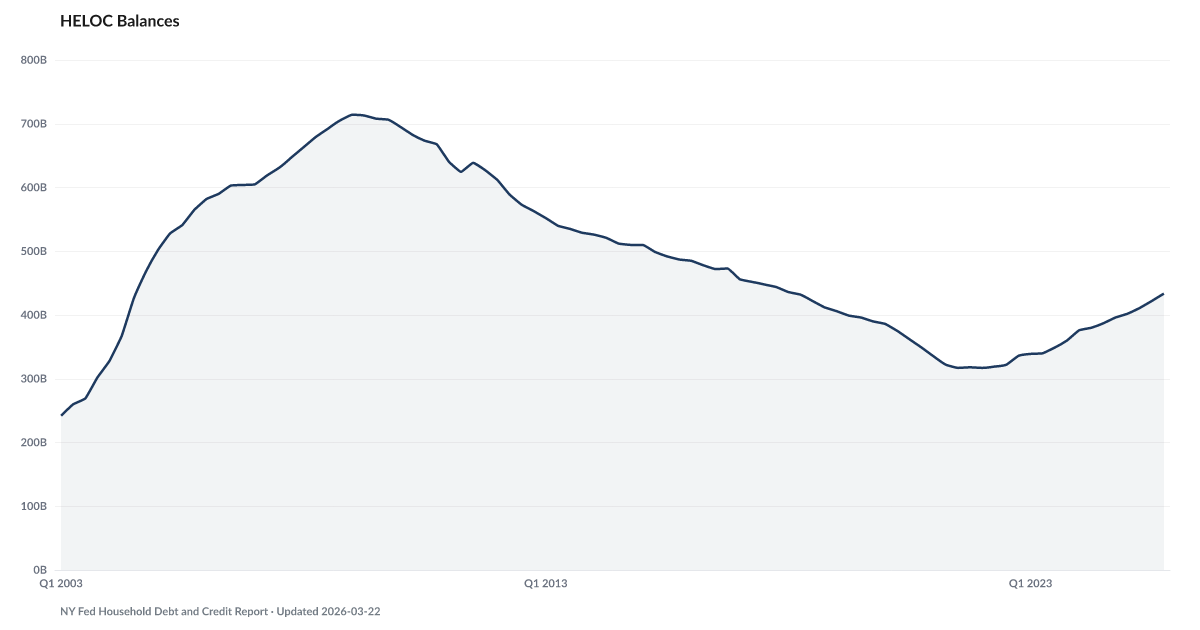

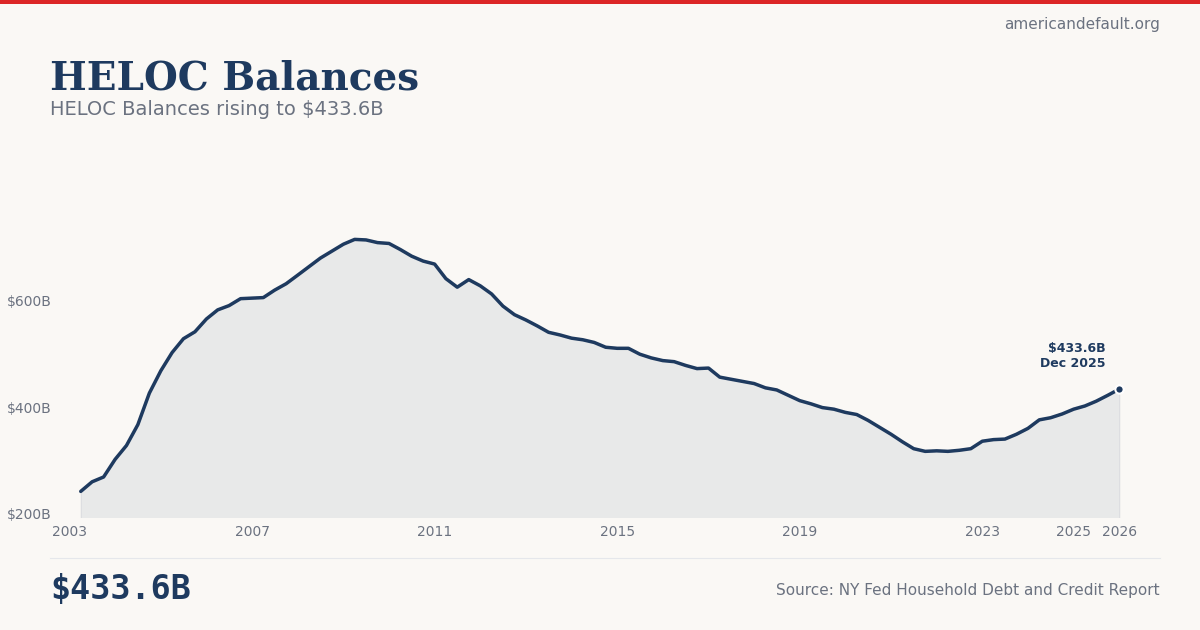

HELOC Balances

Home equity line of credit balances outstanding

What is the current HELOC Balances?

HELOC (Home Equity Line of Credit) balances track how much homeowners have borrowed against their home equity. Rising HELOC balances can indicate that homeowners are tapping accumulated home equity to cover expenses — converting long-term housing wealth into short-term spending capacity. Source: NY Fed Household Debt and Credit Report.

HELOC Balances rising to $433.6B

Tracking worsening relative to recent baseline.

Explore Further

How has HELOC Balances changed over time?

{kind=link}

{kind=link}

| Period | Value | YoY Change |

|---|---|---|

| Q4 2025 | $433.6B | +$37.6B |

| Q3 2025 | $422B | +$35.0B |

| Q2 2025 | $411B | +$31.0B |

| Q1 2025 | $402B | +$26.0B |

| Q4 2024 | $396B | +$36.0B |

| Q3 2024 | $387B | +$38.0B |

| Q2 2024 | $380B | +$40.0B |

| Q1 2024 | $376B | +$37.0B |

| Q4 2023 | $360B | +$24.0B |

| Q3 2023 | $349B | +$27.0B |

| Q2 2023 | $340B | +$21.0B |

| Q1 2023 | $339B | +$22.0B |

Frequently Asked Questions

What are HELOC balances?

HELOCs (Home Equity Lines of Credit) allow homeowners to borrow against the equity in their homes. Rising HELOC balances indicate that more homeowners are tapping their housing wealth, which may signal a need for liquidity as other financial cushions erode.

Why does HELOC growth matter for financial distress?

When homeowners draw on HELOCs to cover current expenses — rather than for home improvements or investments — it parallels the pattern of 401(k) hardship withdrawals: converting long-term assets into short-term spending. It reduces the equity cushion that protects homeowners from underwater mortgages.

Where does HELOC data come from?

The New York Fed reports HELOC balances quarterly in its Household Debt and Credit Report, based on Equifax consumer credit data.

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…