Phantom Debt

$65.3B — up from $54.6B a year ago, invisible to lenders and credit scores

What is the current Phantom Debt?

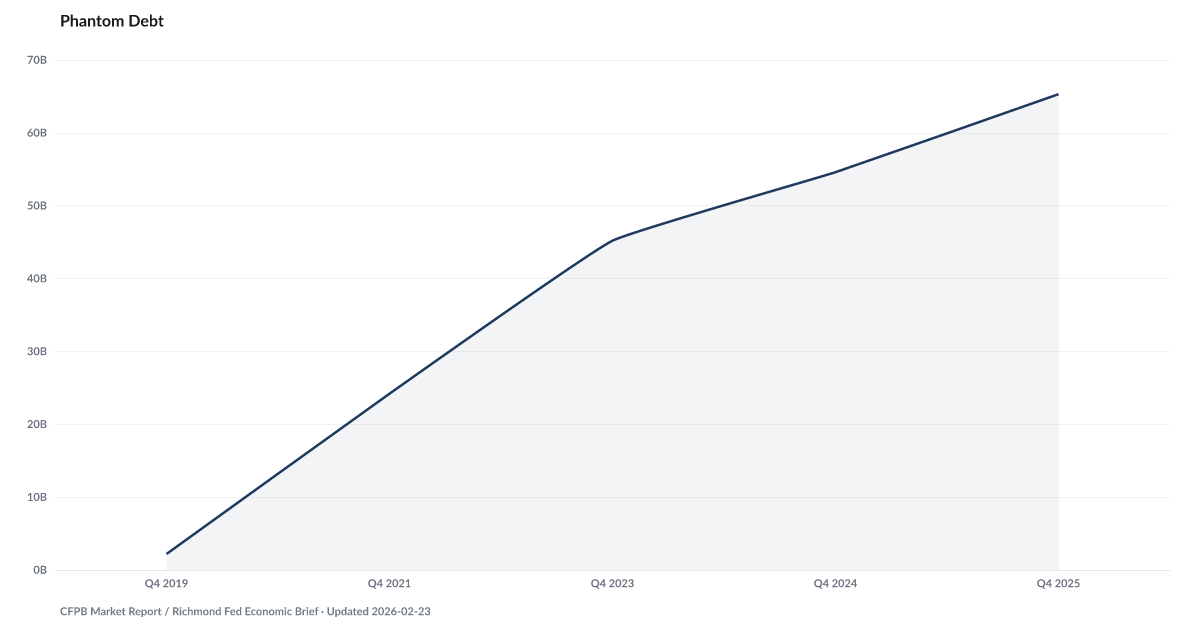

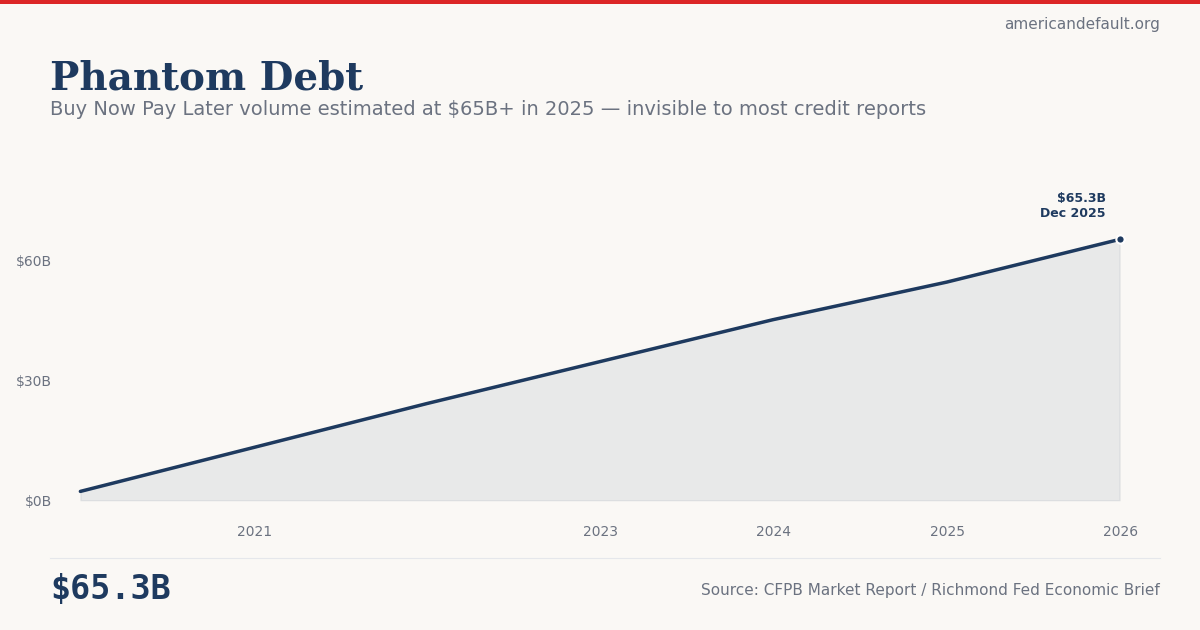

Buy Now Pay Later originations among the six largest lenders reached an estimated $65.3 billion in 2025, according to Richmond Fed projections based on CFPB data — nearly 30 times the $2.2 billion originated in 2019. Most BNPL pay-in-four loans remain invisible to credit bureaus, meaning traditional measures of household debt systematically undercount what families actually owe. Source: Richmond Fed / CFPB (2025).

A $65 billion lending market has grown up almost entirely outside the traditional credit reporting system.

Buy Now Pay Later originations among the six largest lenders reached an estimated $65.3 billion in 2025, according to Richmond Fed projections based on CFPB data. That's nearly 30 times the $2.2 billion originated in 2019. The growth is extraordinary. What makes it different from other forms of consumer credit is that most BNPL pay-in-four loans remain invisible to credit bureaus, meaning traditional measures of household debt systematically undercount what families actually owe.

The CFPB found 53.6 million Americans used BNPL in 2023, and usage continued climbing. The Fed's own 2024 SHED survey found 15% of adults had used BNPL, with nearly 1 in 4 users paying late — up sharply from 18% the prior year. The $400 Test helps explain why: when 37% of adults can't cover a $400 emergency, splitting a $200 purchase into four payments isn't a convenience — it's a necessity.

The outstanding balance at any point is estimated at roughly $3 billion — small compared to the $1.28 trillion tracked by Plastic Ceiling. But BNPL use is concentrated among financially fragile borrowers, the same population already showing stress in Falling Behind, where total delinquency has risen to 4.8%. Adding an invisible layer of obligations to already-strained households creates risk that lenders and regulators literally cannot see.

Explore Further

Is this happening to you?

Are you using buy-now-pay-later to spread out purchases you used to pay for upfront?

How has Phantom Debt changed over time?

{kind=link}

{kind=link}

| Period | Value | YoY Change |

|---|---|---|

| 2025 | $65.3B | +$10.7B |

| 2024 | $54.6B | +$9.4B |

| 2023 | $45.2B | — |

| 2021 | $24.2B | — |

| 2019 | $2.2B | — |

Frequently Asked Questions

How large is the Buy Now Pay Later market?

BNPL originations reached an estimated $65.3 billion in 2025 among the six largest lenders, according to Richmond Fed projections based on CFPB data. This is nearly 30 times the $2.2 billion originated in 2019. The CFPB found 53.6 million Americans used BNPL in 2023, with usage continuing to climb.

Why is BNPL called 'phantom debt'?

Most BNPL pay-in-four loans are not reported to credit bureaus, meaning they do not appear on credit reports or factor into credit scores. This makes BNPL obligations invisible to traditional measures of household debt. Lenders making new credit decisions cannot see a borrower's existing BNPL commitments.

What is the BNPL delinquency rate?

The Fed's 2024 SHED survey found that nearly 1 in 4 BNPL users (24%) reported paying late — up sharply from 18% the prior year. Because most BNPL delinquencies are not reported to credit bureaus, they do not appear in traditional delinquency statistics.

Who uses Buy Now Pay Later?

BNPL use is concentrated among financially fragile borrowers. The Fed's SHED survey found that 15% of all adults had used BNPL, but usage is higher among those who cannot cover a $400 emergency. For these borrowers, BNPL is not a convenience — it is a necessity for purchasing basic items.

Where does the BNPL data come from?

American Default tracks BNPL using Richmond Fed projections based on CFPB regulatory data from the six largest BNPL lenders. Additional data comes from the Fed's annual SHED survey, which asks households directly about BNPL usage and payment behavior.

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…