The $400 Test

37% — unchanged from a year ago; 1 in 3 adults still can't cover it with cash

What is the current The $400 Test?

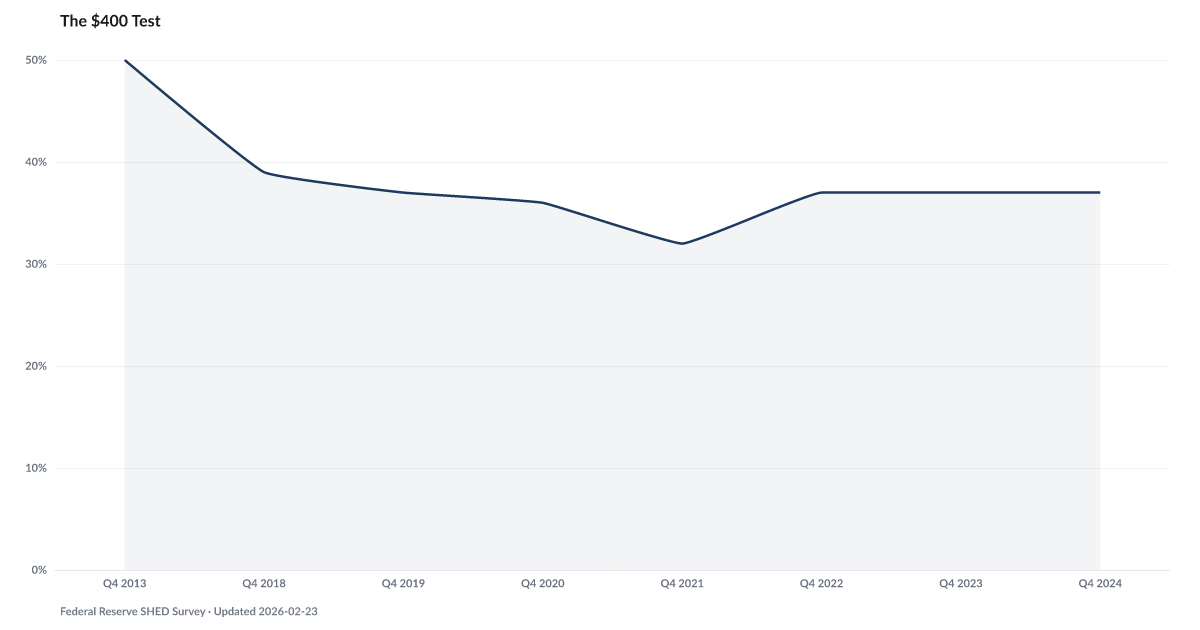

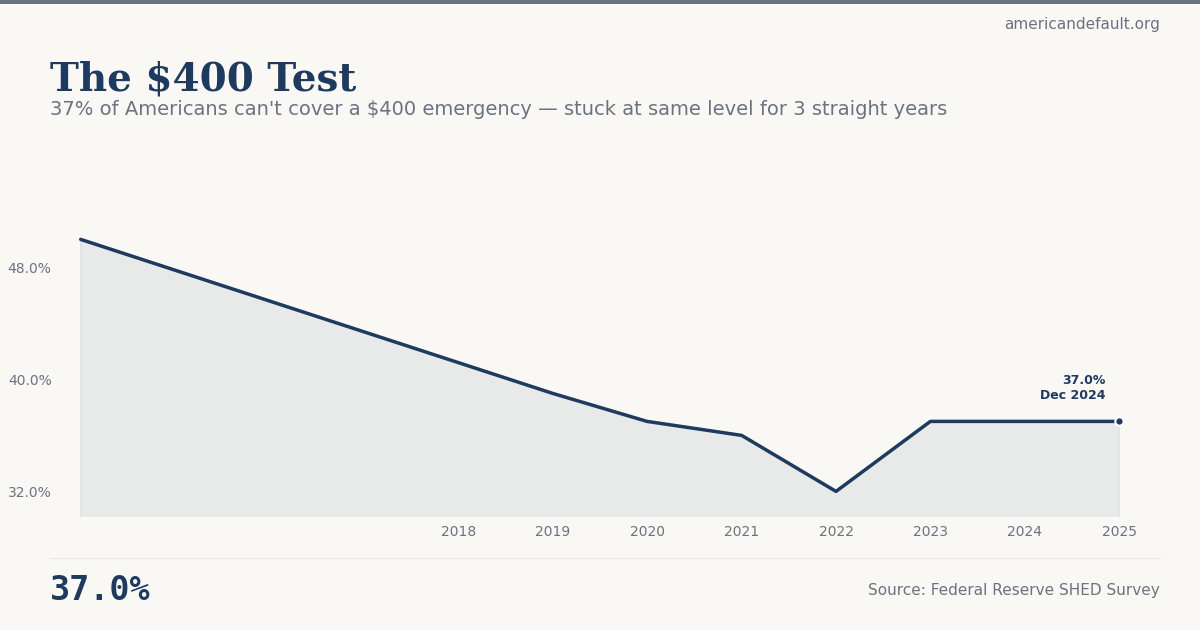

37% of American adults could not cover a $400 emergency expense using cash or its equivalent in 2024, according to the Federal Reserve's Survey of Household Economics and Decisionmaking (SHED). This figure has been essentially unchanged for three consecutive years, after briefly improving to 32% in 2021 when stimulus payments temporarily rebuilt household reserves. Source: Federal Reserve SHED (published May 2025).

The Federal Reserve has asked the same question for over a decade, and the answer has stopped improving.

The Fed's Survey of Household Economics and Decisionmaking, fielded in October 2024 and published in May 2025, found that 37% of American adults could not cover a $400 emergency expense using cash or its equivalent. That figure has been essentially unchanged — 37% — for three consecutive years, after briefly falling to 32% in 2021 when stimulus payments temporarily rebuilt household reserves.

The plateau is more troubling than a spike would be. A spike suggests a crisis that might pass. A plateau at 37% suggests a structural floor — a share of the population that simply cannot accumulate even minimal savings regardless of labor market conditions. The Safety Net confirms it from a different survey: only 41% of Americans would use savings for a $1,000 emergency. Two surveys, two methodologies, the same conclusion.

What these households use instead of savings is visible in Phantom Debt — Buy Now Pay Later volume has exploded from $2.2 billion in 2019 to $65.3 billion in 2025, with the Fed's own SHED finding that 24% of BNPL users are paying late. The Squeeze connects the mechanism: 24% of households spend 95% or more of income on necessities, leaving nothing to save.

The $400 test was designed to measure financial fragility. At 37%, it's measuring something closer to a permanent condition.

Explore Further

Is this happening to you?

Could you handle a $400 unexpected expense right now?

How has The $400 Test changed over time?

{kind=link}

{kind=link}

| Period | Value | YoY Change |

|---|---|---|

| 2024 | 37% | +0.0 pts |

| 2023 | 37% | +0.0 pts |

| 2022 | 37% | +5.0 pts |

| 2021 | 32% | −4.0 pts |

| 2020 | 36% | −1.0 pts |

| 2019 | 37% | −2.0 pts |

| 2018 | 39% | — |

| 2013 | 50% | — |

Frequently Asked Questions

What percentage of Americans can't cover a $400 emergency?

37% of American adults could not cover a $400 emergency expense using cash or its equivalent in 2024, according to the Federal Reserve's Survey of Household Economics and Decisionmaking. This has been essentially flat for three consecutive years.

Has the $400 emergency savings figure improved over time?

It briefly improved to 32% in 2021 when stimulus payments rebuilt household reserves, but has since reverted to 37% and plateaued there. The Fed has asked this question annually since 2013. The plateau at 37% suggests a structural floor — a share of the population that cannot accumulate even minimal savings regardless of labor market conditions.

What do people use instead of savings for emergencies?

Those without cash savings typically borrow (credit cards, personal loans), sell possessions, use Buy Now Pay Later services, or skip the expense entirely. Buy Now Pay Later volume has grown from $2.2 billion in 2019 to $65.3 billion in 2025, with 24% of BNPL users paying late according to the Fed's own SHED survey.

What is the Fed SHED survey?

The Survey of Household Economics and Decisionmaking (SHED) is an annual Federal Reserve survey measuring the financial well-being of U.S. households. It is fielded in October–November and published the following May. The $400 emergency question has become one of its most widely cited findings.

How does the $400 Test relate to the American Distress Index?

The $400 Test is part of the Buffer Depletion dimension of the American Distress Index, which carries 30% of the total weight. It provides household-level confirmation of what the macro savings rate shows: American financial cushions have eroded to the point where minor expenses can trigger cascading financial distress.

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…