The Spread

Up from 29 a year ago, credit card trouble spreading geographically

What is the current The Spread?

The number of U.S. states where credit card delinquency exceeds 10% is a geographic concentration measure of household debt distress. When delinquency crosses 10% at the state level, it indicates that debt problems have spread beyond individual borrowers to affect the broader regional economy. Source: NY Fed Consumer Credit Panel.

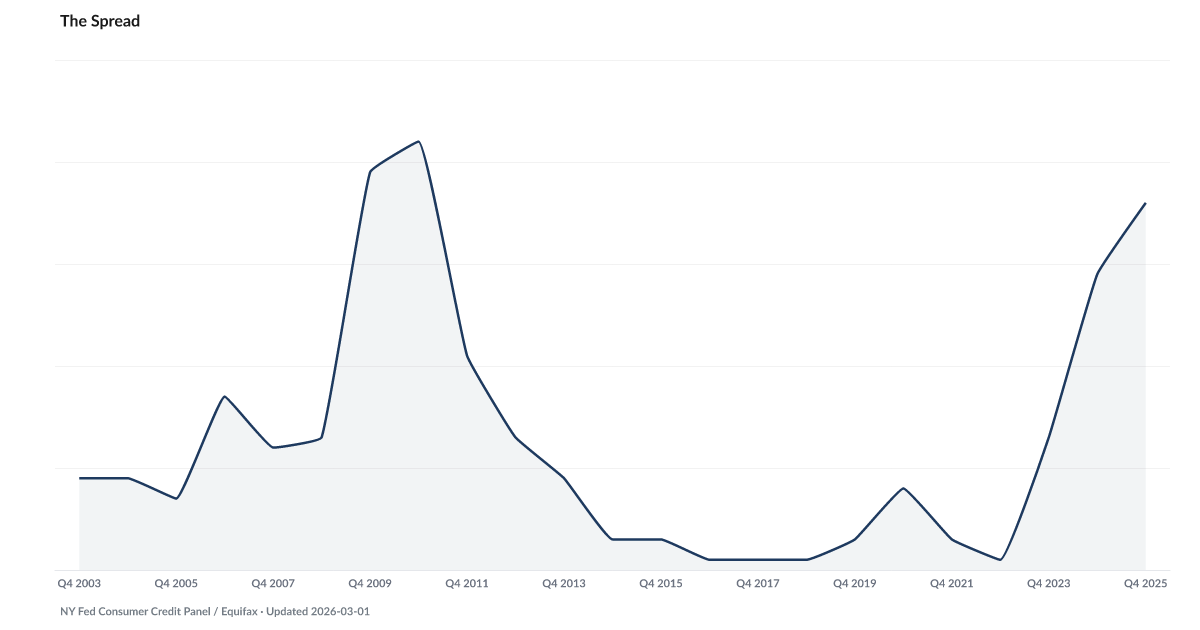

The number of states where credit card delinquency crosses 10% has climbed from one state in 2018 to 36 in 2025, 14% below the Great Recession high.

The New York Fed's Consumer Credit Panel, built from Equifax data, tracks credit card delinquency state by state. In 2016, exactly one state was above the 10% threshold. In 2019, three. In 2025, 36.

That is a national deterioration, not a regional one. The old story of credit distress concentrated in a handful of Sun Belt foreclosure markets no longer fits. The stress is in New York and Texas and Ohio and Georgia at once.

During the Great Recession, the state count set the comparison point. The current reading is 14% below that recession-era high while the official unemployment rate remains historically low.

Falling Behind provides the national aggregate, while this page shows how many states have crossed the named delinquency threshold. The Buffer and The Squeeze provide separate savings and necessities context. The co-movement is descriptive here; it is not presented as a validated lead-lag relationship.

Explore Further

How has The Spread changed over time?

Most affected counties

Counties with the highest safety net and buffer scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| 2025 | 36 | +7.00 |

| 2024 | 29 | +16.00 |

| 2023 | 13 | +12.00 |

| 2022 | 1 | −2.00 |

| 2021 | 3 | −5.00 |

| 2020 | 8 | +5.00 |

| 2019 | 3 | +2.00 |

| 2018 | 1 | +0.00 |

| 2017 | 1 | +0.00 |

| 2016 | 1 | −2.00 |

| 2015 | 3 | +0.00 |

| 2014 | 3 | −6.00 |

Frequently Asked Questions

How many states have credit card delinquency above 10%?

The count of states exceeding the 10% credit card delinquency threshold is tracked quarterly using New York Fed Consumer Credit Panel data. A rising count indicates that debt distress is spreading geographically rather than being concentrated in a few regions.

Why does geographic spread matter?

Concentrated distress can be managed — states and institutions can absorb localized problems. When delinquency rises above 10% in multiple states simultaneously, it indicates systemic rather than regional stress, reducing the capacity of any single policy response to address the problem.

Where does the state-level delinquency data come from?

The New York Fed's Consumer Credit Panel provides quarterly credit performance data at the state level, drawn from a nationally representative sample of Equifax credit reports.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…