The Other Banks

Credit card delinquency at smaller community banks

What is the current The Other Banks?

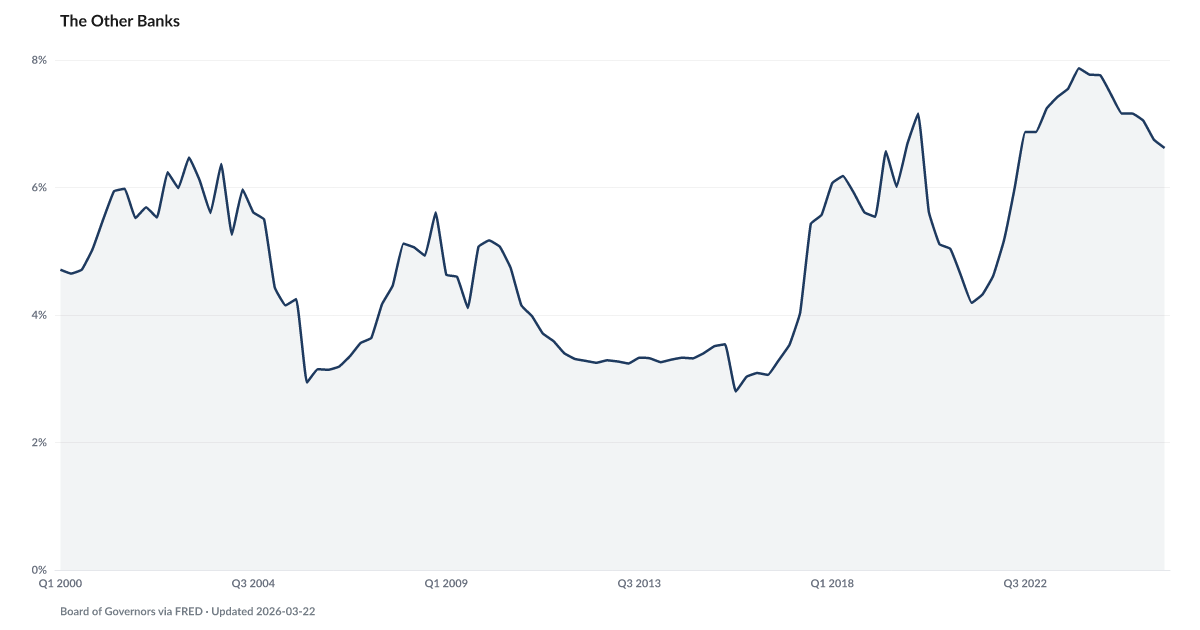

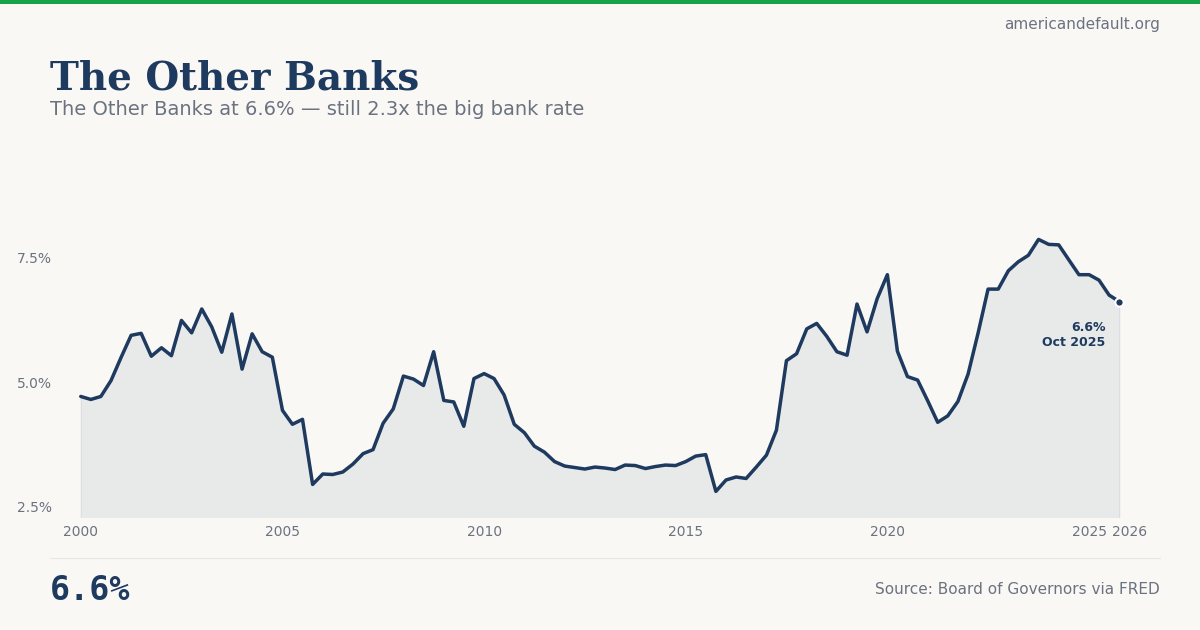

Credit card delinquency at banks outside the top 100 — community banks, regional lenders, and credit unions — stood at 6.62% in Q4 2025, according to Federal Reserve data. This is more than double the 2.84% rate at the nation's 100 largest banks. The 3.78 percentage point gap reflects two fundamentally different lending environments operating within the same economy. Source: Federal Reserve Call Reports (Q4 2025).

Behind the headline banking numbers, a parallel credit system serving smaller communities is showing far deeper distress.

Credit card delinquency at banks outside the top 100 — community banks, regional lenders, and credit unions — stood at 6.62% in Q4 2025, according to Federal Reserve data. That's more than double the 2.84% rate at the nation's 100 largest banks. The gap, currently at 3.78 percentage points, reflects two fundamentally different lending environments operating within the same economy.

The divergence isn't new, but it has persisted at elevated levels since 2017 when small bank delinquency surged from around 3% to over 5%. Plastic Ceiling shows total credit card debt at $1.28 trillion — but the risk is not evenly distributed. Smaller banks serve borrowers who are less likely to qualify for prime rates at major institutions, meaning they're carrying debt at even higher effective interest rates than the 20.97% average tracked by The Card Tax.

This indicator is a canary in two senses. First, it shows stress among the most financially fragile borrowers before it shows up in headline numbers. Second, it reveals risk in the banking system itself: smaller institutions have less capacity to absorb losses. Falling Behind shows the aggregate delinquency rate climbing to 4.8%, but that average masks a story of deeply uneven stress.

Explore Further

Is this happening to you?

Do you carry a credit card balance from month to month?

How has The Other Banks changed over time?

{kind=link}

{kind=link}

| Period | Value | YoY Change |

|---|---|---|

| Q4 2025 | 6.62% | −0.5 pts |

| Q3 2025 | 6.75% | −0.7 pts |

| Q2 2025 | 7.05% | −0.7 pts |

| Q1 2025 | 7.16% | −0.6 pts |

| Q4 2024 | 7.16% | −0.7 pts |

| Q3 2024 | 7.46% | −0.1 pts |

| Q2 2024 | 7.76% | +0.3 pts |

| Q1 2024 | 7.77% | +0.5 pts |

| Q4 2023 | 7.87% | +1.0 pts |

| Q3 2023 | 7.55% | +0.7 pts |

| Q2 2023 | 7.42% | +1.4 pts |

| Q1 2023 | 7.24% | +2.1 pts |

Frequently Asked Questions

How does credit card delinquency differ between large and small banks?

Credit card delinquency at banks outside the top 100 was 6.62% in Q4 2025, more than double the 2.84% rate at the nation's 100 largest banks. The gap of 3.78 percentage points reflects the different borrower populations these institutions serve.

Why is small bank delinquency so much higher?

Smaller banks serve borrowers who are less likely to qualify for prime rates at major institutions. These borrowers carry debt at even higher effective interest rates and have thinner financial buffers. They are the most financially fragile segment of the credit market.

Why does the large-vs-small bank gap matter?

The gap reveals that headline delinquency averages mask deeply uneven stress. It also flags risk in the banking system: smaller institutions have less capacity to absorb losses than the largest banks. Stress among these borrowers and lenders can be a leading indicator of broader credit market problems.

Is the gap between large and small bank delinquency widening?

The divergence has persisted at elevated levels since 2017, when small bank delinquency surged from around 3% to over 5%. The gap has remained wide since, suggesting a structural rather than cyclical difference in the financial health of borrowers served by different parts of the banking system.

Where does the large vs. small bank delinquency data come from?

The Federal Reserve publishes delinquency rates separately for the 100 largest banks and all other banks based on quarterly Call Report filings. This allows comparison of credit performance across different tiers of the banking system.

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…