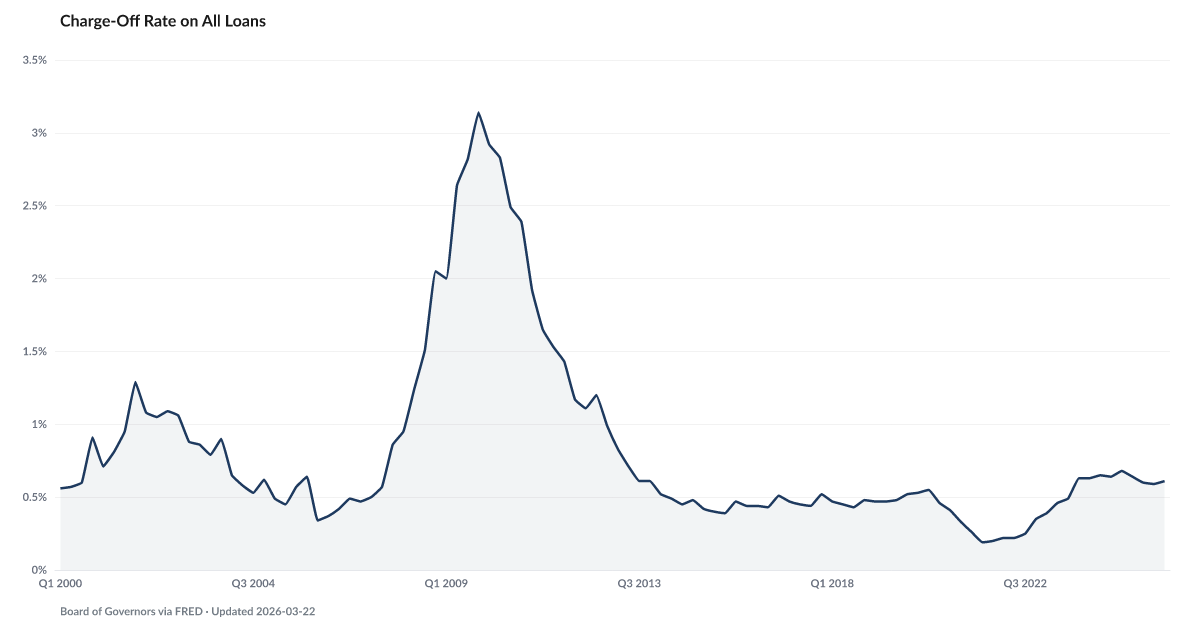

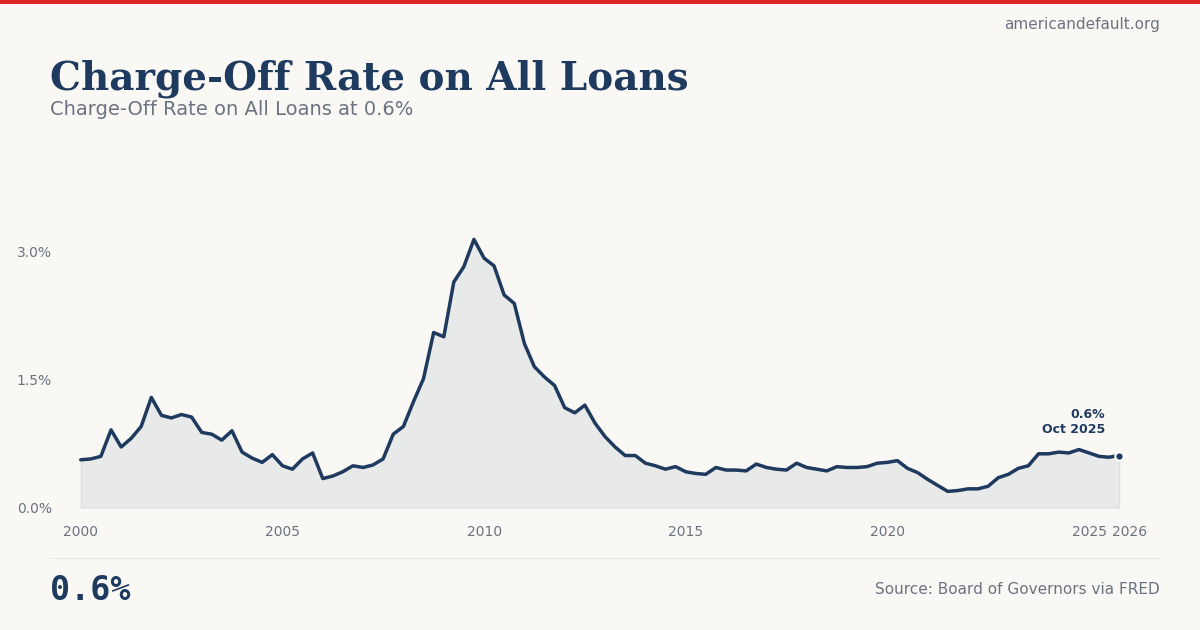

Charge-Off Rate on All Loans

All consumer loans written off as uncollectable

Delinquency Rate on Credit Card Loans is currently elevated — historically leads this indicator by 3 quarters. Delinquency Rate on Credit Card Loans · View projections

What is the current Charge-Off Rate on All Loans?

The charge-off rate on all loans at commercial banks was 0.61% in the latest quarter, according to the Federal Reserve. Charge-offs represent debt that banks have written off as uncollectible — the final stage of the default cycle. Rising charge-offs confirm that delinquencies are translating into actual losses. Source: Federal Reserve via FRED (CORALACBN).

Charge-Off Rate on All Loans at 0.6%

Tracking improving relative to recent baseline.

Explore Further

How has Charge-Off Rate on All Loans changed over time?

{kind=link}

{kind=link}

| Period | Value | YoY Change |

|---|---|---|

| Q4 2025 | 0.61% | −0.1 pts |

| Q3 2025 | 0.59% | −0.1 pts |

| Q2 2025 | 0.6% | −0.1 pts |

| Q1 2025 | 0.64% | +0.0 pts |

| Q4 2024 | 0.68% | +0.1 pts |

| Q3 2024 | 0.64% | +0.2 pts |

| Q2 2024 | 0.65% | +0.2 pts |

| Q1 2024 | 0.63% | +0.2 pts |

| Q4 2023 | 0.63% | +0.3 pts |

| Q3 2023 | 0.49% | +0.2 pts |

| Q2 2023 | 0.46% | +0.2 pts |

| Q1 2023 | 0.39% | +0.2 pts |

Frequently Asked Questions

What is the charge-off rate on all loans?

The charge-off rate measures the percentage of total loans that banks write off as uncollectible losses. At 0.61%, it reflects the aggregate loss rate across all commercial bank loan portfolios.

Why do charge-offs matter?

Charge-offs are the end of the default pipeline: delinquency → serious delinquency → charge-off. Rising charge-offs confirm that earlier delinquency signals have translated into actual bank losses.

Where does this data come from?

Published quarterly by the Federal Reserve Board, available via FRED series CORALACBN.

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…