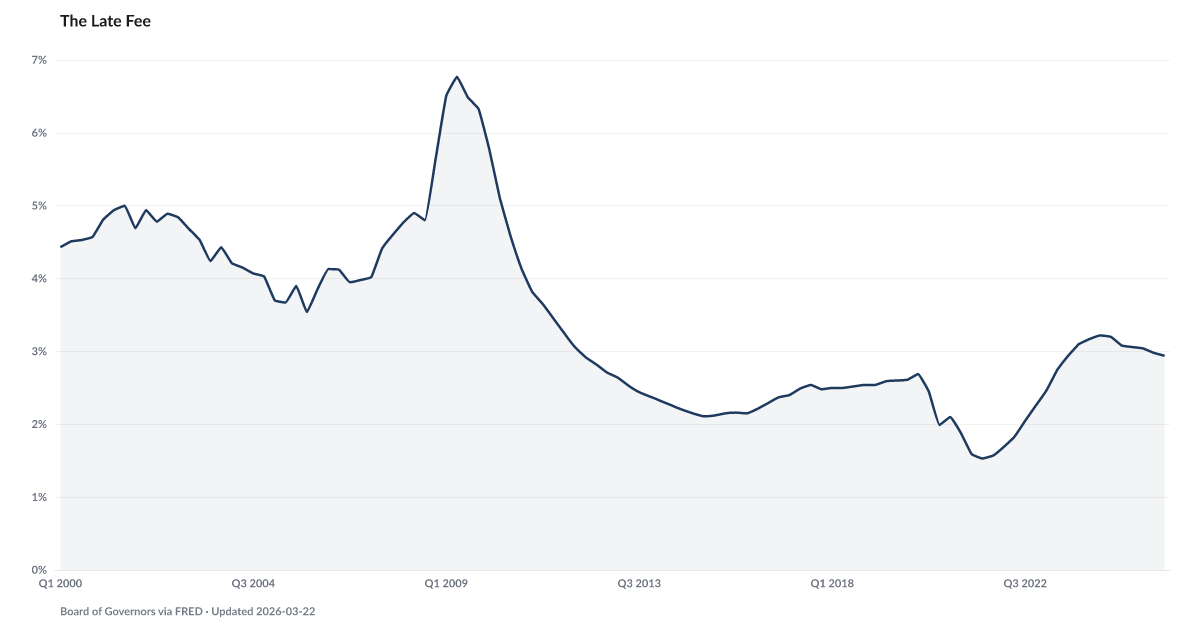

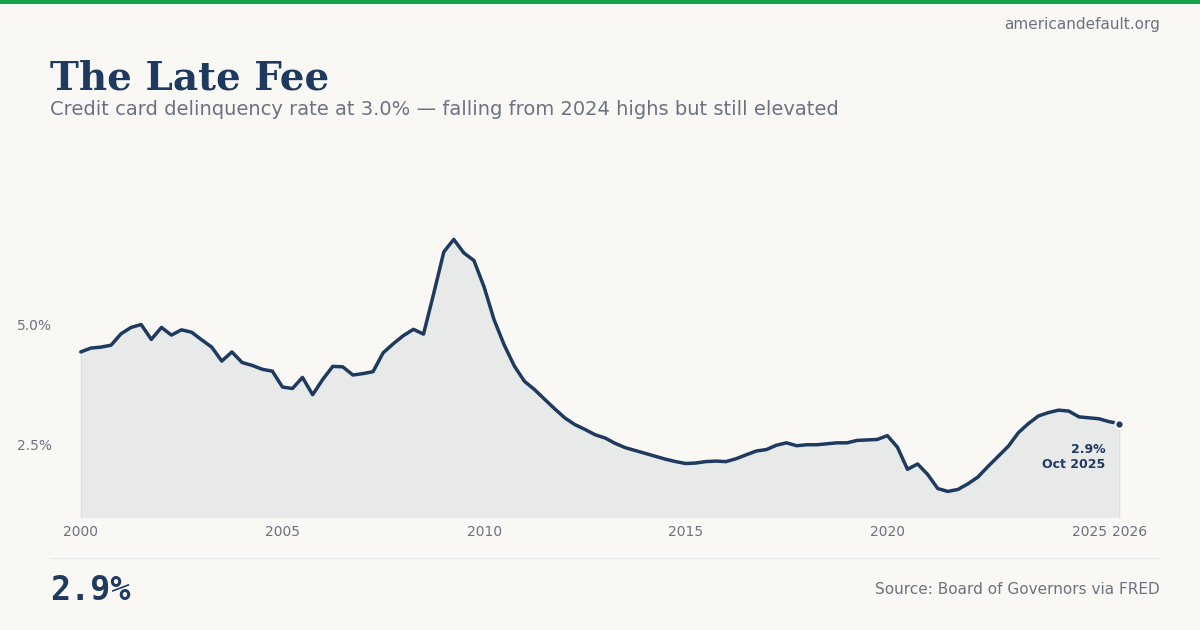

The Late Fee

Tracking improving relative to recent baseline.

Currently elevated — historically leads Charge-Off Rate on All Loans by 3 quarters. Charge-Off Rate on All Loans · View projections

What is the current The Late Fee?

The U.S. credit card delinquency rate was 2.94% in Q4 2025, according to the Federal Reserve Board — down slightly from the 2024 high of 3.24% but still well above the pre-pandemic norm of roughly 2.5%. Rising credit card delinquency is a component of the American Distress Index's Debt Stress dimension and signals that a growing share of households cannot keep up with minimum payments. Source: Federal Reserve via FRED (DRCCLACBS).

Credit card delinquency rate at 3.0% — falling from 2024 highs but still elevated

Tracking improving relative to recent baseline.

Explore Further

How has The Late Fee changed over time?

{kind=link}

{kind=link}

| Period | Value | YoY Change |

|---|---|---|

| Q4 2025 | 2.94% | −0.1 pts |

| Q3 2025 | 2.98% | −0.2 pts |

| Q2 2025 | 3.04% | −0.2 pts |

| Q1 2025 | 3.06% | −0.1 pts |

| Q4 2024 | 3.08% | −0.0 pts |

| Q3 2024 | 3.2% | +0.3 pts |

| Q2 2024 | 3.22% | +0.5 pts |

| Q1 2024 | 3.17% | +0.7 pts |

| Q4 2023 | 3.1% | +0.8 pts |

| Q3 2023 | 2.94% | +0.9 pts |

| Q2 2023 | 2.75% | +0.9 pts |

| Q1 2023 | 2.47% | +0.8 pts |

Frequently Asked Questions

What is the current credit card delinquency rate?

The credit card delinquency rate was 2.94% in Q4 2025, according to the Federal Reserve Board. This is down from the recent high of 3.24% in Q4 2024 but remains above the pre-pandemic average of approximately 2.5%.

What does credit card delinquency measure?

Credit card delinquency measures the share of credit card balances at least 30 days past due. The Federal Reserve publishes this quarterly as the "Delinquency Rate on Credit Card Loans, All Commercial Banks" (FRED series DRCCLACBS). Rising delinquency means more households cannot keep up with minimum payments.

Why is credit card delinquency elevated compared to pre-pandemic?

Two forces drove delinquency above pre-pandemic levels: record credit card balances (over $1.2 trillion) and interest rates near 20-year highs (averaging 21%+). When savings buffers ran out and rates rose, more households fell behind on minimum payments. The American Distress Index tracks this as part of its Debt Stress component.

How does credit card delinquency connect to the American Distress Index?

Credit card delinquency is a component of the Debt Stress dimension in the American Distress Index, which carries 25% of the composite score. The ADI's Buffer Depletion dimension (savings rates) typically leads Debt Stress by 9 quarters, meaning delinquency rises after savings fall — a pattern validated in the 2007-2010 crisis.

Where does credit card delinquency data come from?

The Federal Reserve Board publishes credit card delinquency rates quarterly as part of its Charge-Off and Delinquency Rates on Loans and Leases at Commercial Banks report. American Default tracks this via the FRED series DRCCLACBS, updated with a one-quarter lag.

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…