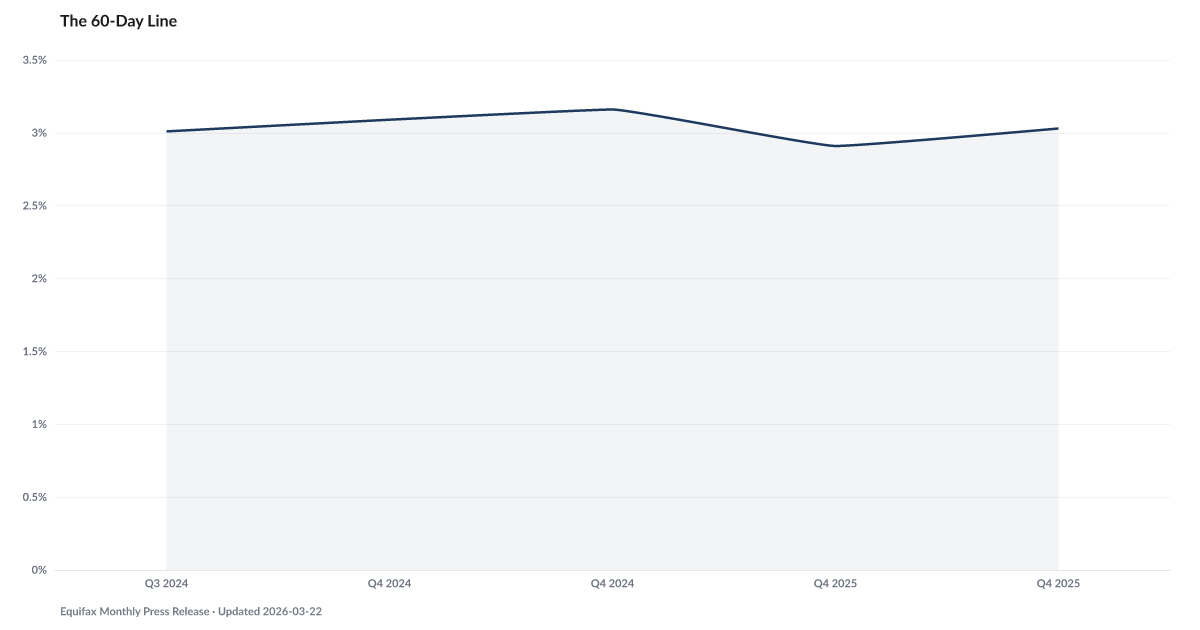

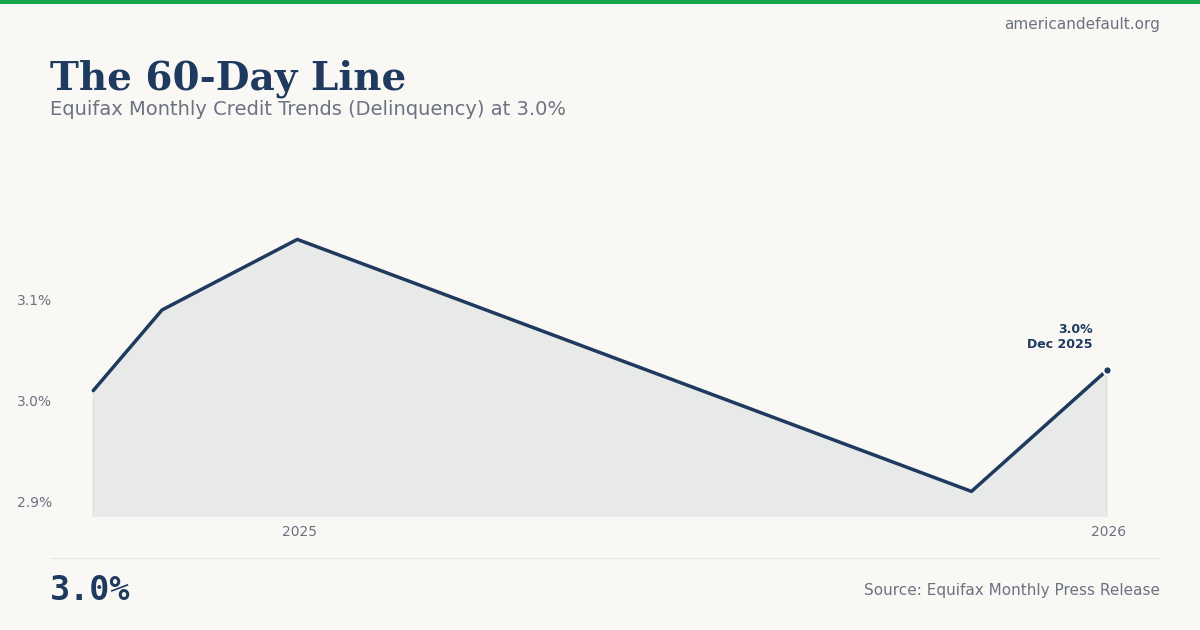

The 60-Day Line

3.03% — up from 2.91% last quarter; bankcard 60+ day delinquency still climbing

What is the current The 60-Day Line?

Equifax Monthly Credit Trends tracks early-stage delinquency transitions across consumer credit portfolios, providing a near-real-time view of payment deterioration. The 60-day delinquency marker is a critical threshold — accounts that reach 60 days past due have a substantially higher probability of progressing to charge-off than those at 30 days. Source: Equifax credit data.

Equifax Monthly Credit Trends (Delinquency) at 3.0%

Tracking improving relative to recent baseline.

Explore Further

Is this happening to you?

Have any of your accounts gone 60 or more days past due?

How has The 60-Day Line changed over time?

{kind=link}

{kind=link}

| Period | Value | YoY Change |

|---|---|---|

| Dec 2025 | 3.03% | −0.1 pts |

| Oct 2025 | 2.91% | −0.2 pts |

| Dec 2024 | 3.16% | — |

| Oct 2024 | 3.09% | — |

| Sep 2024 | 3.01% | — |

Frequently Asked Questions

What does the 60-day delinquency line measure?

It tracks the share of consumer credit accounts that have transitioned to 60+ days past due. The 60-day mark is significant because accounts reaching this stage have a substantially higher probability of progressing to charge-off (total loss) than those at only 30 days past due.

Why is 60 days a critical threshold?

At 30 days past due, many borrowers recover. At 60 days, the probability of recovery drops sharply and the likelihood of eventual charge-off or collections increases significantly. The 60-day line is where temporary cash-flow problems become entrenched delinquency.

Where does this data come from?

Equifax publishes monthly credit trend data from its consumer credit database. As one of the three major credit bureaus, Equifax covers hundreds of millions of consumer credit accounts.

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…