First Missed

Back down after a brief uptick; early-stage mortgage trouble remains low by historical standards

What is the current First Missed?

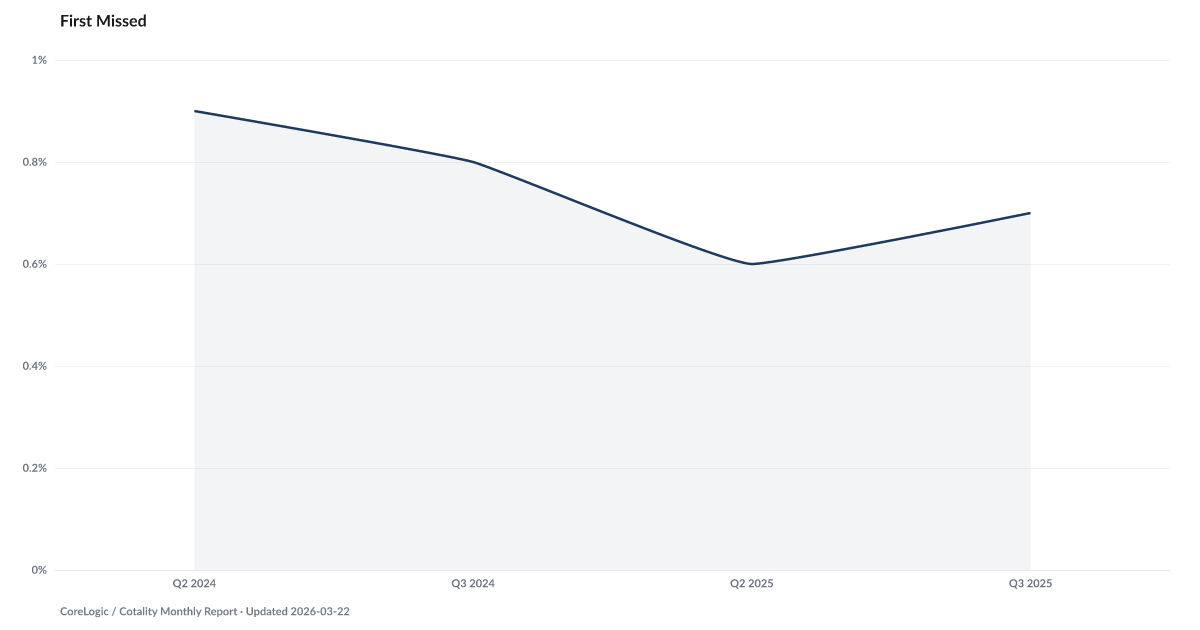

CoreLogic's early-stage transition data tracks the rate at which current mortgages move to 30-day delinquency for the first time — the earliest measurable signal in the mortgage distress pipeline. A rising transition rate indicates that homeowners who were previously current are beginning to fall behind, often months before these mortgages appear in standard delinquency statistics. Source: CoreLogic Early-Stage Delinquency Transitions.

The share of mortgage borrowers making their first missed payment has drifted up from its 2025 low, the earliest tremor in a housing book that otherwise looks calm.

Every foreclosure begins as a single missed payment.

CoreLogic tracks that moment directly — the share of borrowers who were current last month and are 30 days late this month. It is the earliest measurable point in the mortgage distress pipeline, the tripwire that fires before every later stage. In Q1 2026 the rate was 0.6%, up from its 2025 low.

That movement is small. It also matters. Mortgage Delinquency at the 90-day mark has been historically quiet and looks reassuringly calm. But the 90-day figure is the output of whatever happened in the first-missed series three quarters ago. The pipeline runs in one direction.

Most of the borrowers who miss a first payment cure within 90 days. The rest move into the pipeline that eventually produces Foreclosure Starts. A small uptick in first-missed will not show up in mortgage charge-offs for another year or two, which is why reading this indicator alongside the quiet 90-day series is the whole point.

Explore Further

Is this happening to you?

Did you miss your first mortgage payment recently?

How has First Missed changed over time?

Most affected counties

Counties with the highest default and legal scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q1 2026 | 0.6% | +0.0 pts |

| Q4 2025 | 0.7% | — |

| Q3 2025 | 0.7% | −0.1 pts |

| Q2 2025 | 0.6% | −0.3 pts |

| Q1 2025 | 0.6% | — |

| Q3 2024 | 0.8% | — |

| Q2 2024 | 0.9% | — |

Frequently Asked Questions

What does the early-stage transition rate measure?

It measures the rate at which current (performing) mortgages transition to 30-day delinquency for the first time. This is the earliest measurable signal in the mortgage default pipeline, capturing new distress before it shows up in standard delinquency statistics.

Why is this an early warning indicator?

Standard delinquency rates count all loans that are behind — including those already deep in the default pipeline. The early-stage transition rate specifically isolates new delinquencies, showing whether the rate of new households falling behind is accelerating or decelerating.

Where does this data come from?

CoreLogic tracks mortgage performance data from its loan-level database, which covers a large share of the U.S. mortgage market. Early-stage transition metrics are published in CoreLogic's monthly Loan Performance Insights reports.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…